Q4FY26 Earnings Review

Date: 3rd June, 2026

The Q4 FY26 corporate earnings season marked a differentiated performance by corporates. Excluding one-offs large caps struggled for net profit growth while mid-caps posted a resilient performance with mid-twenties PAT growth. However, this performance gets clouded by continuing geopolitical tensions in the Middle East and deficit monsoon forecasts.

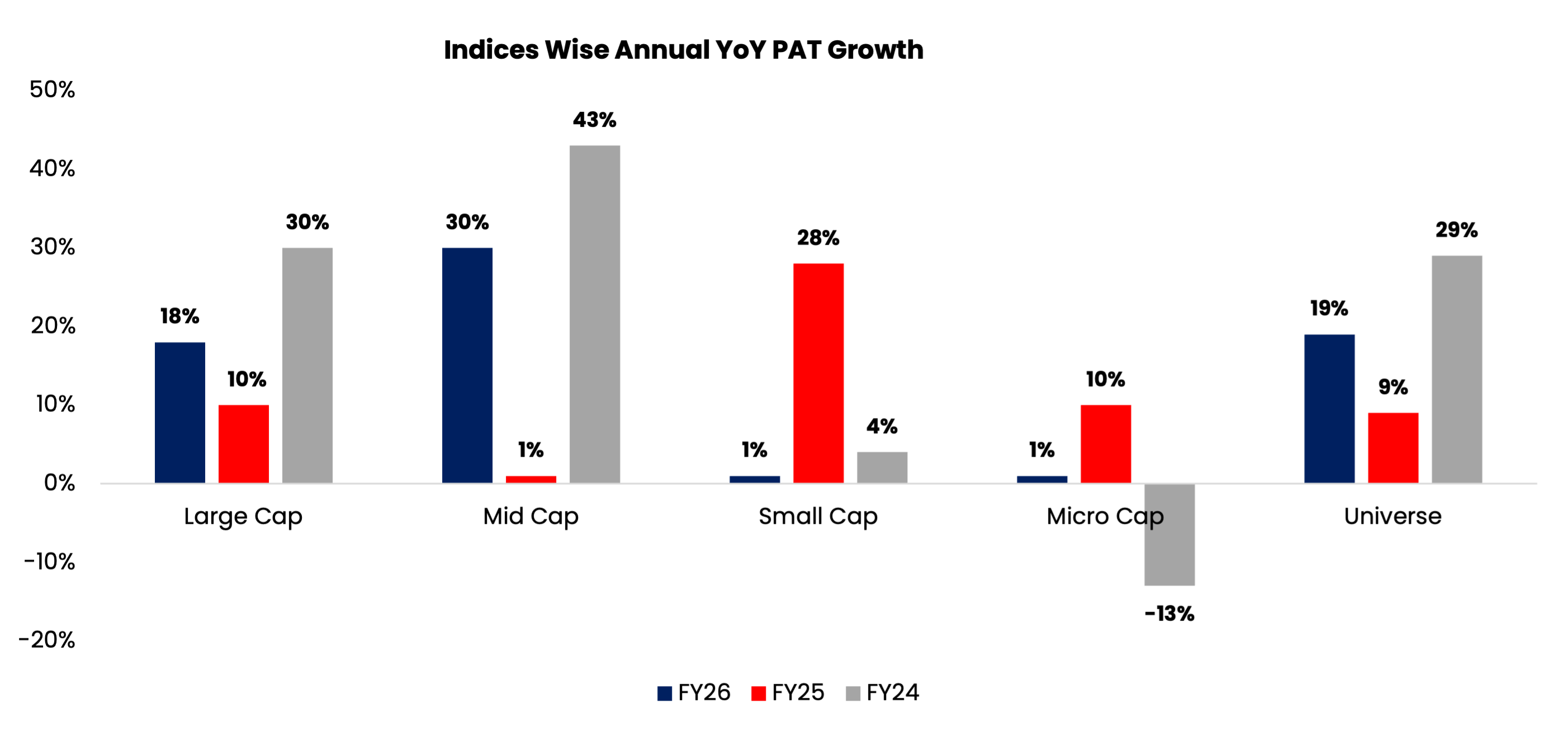

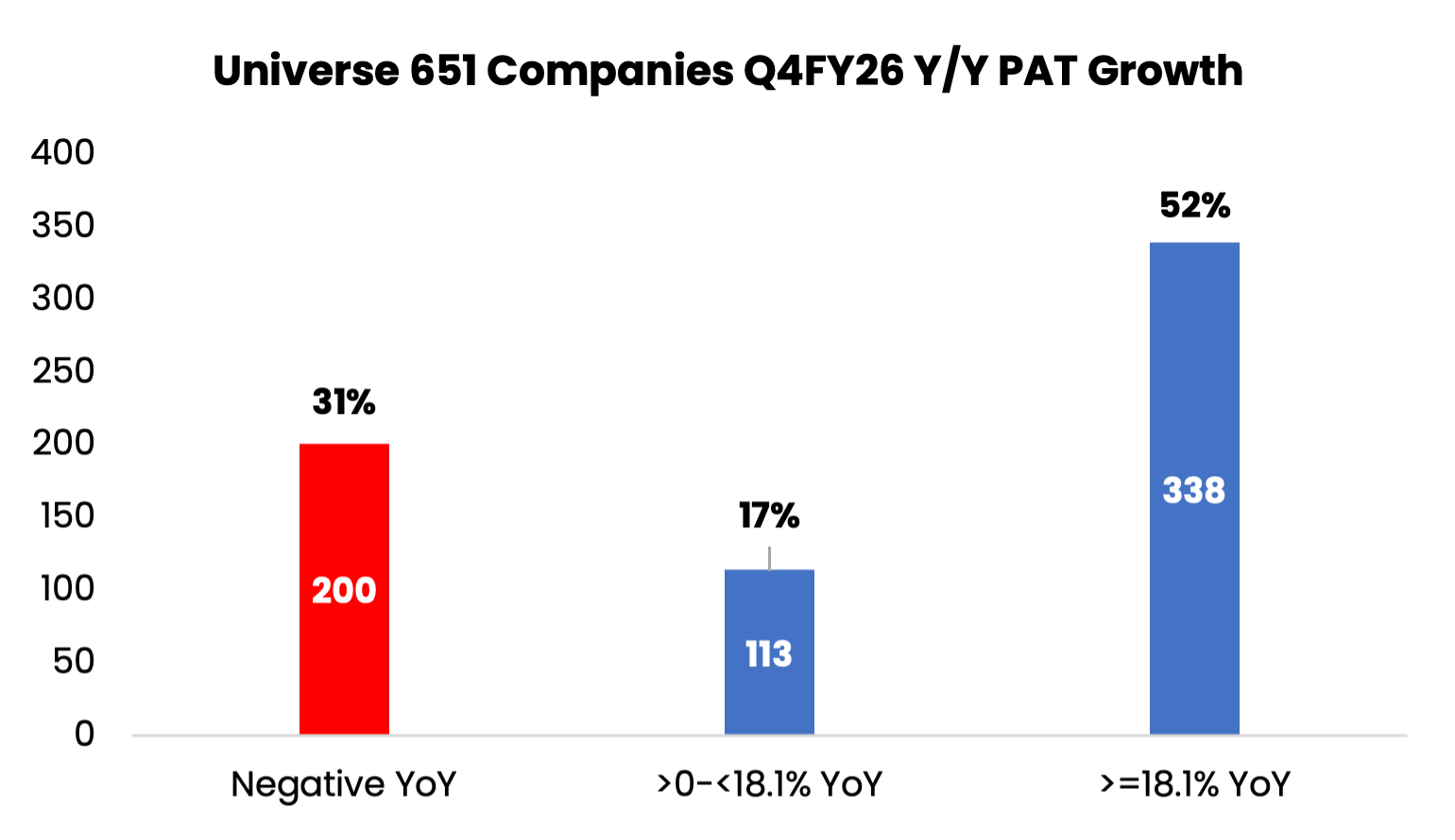

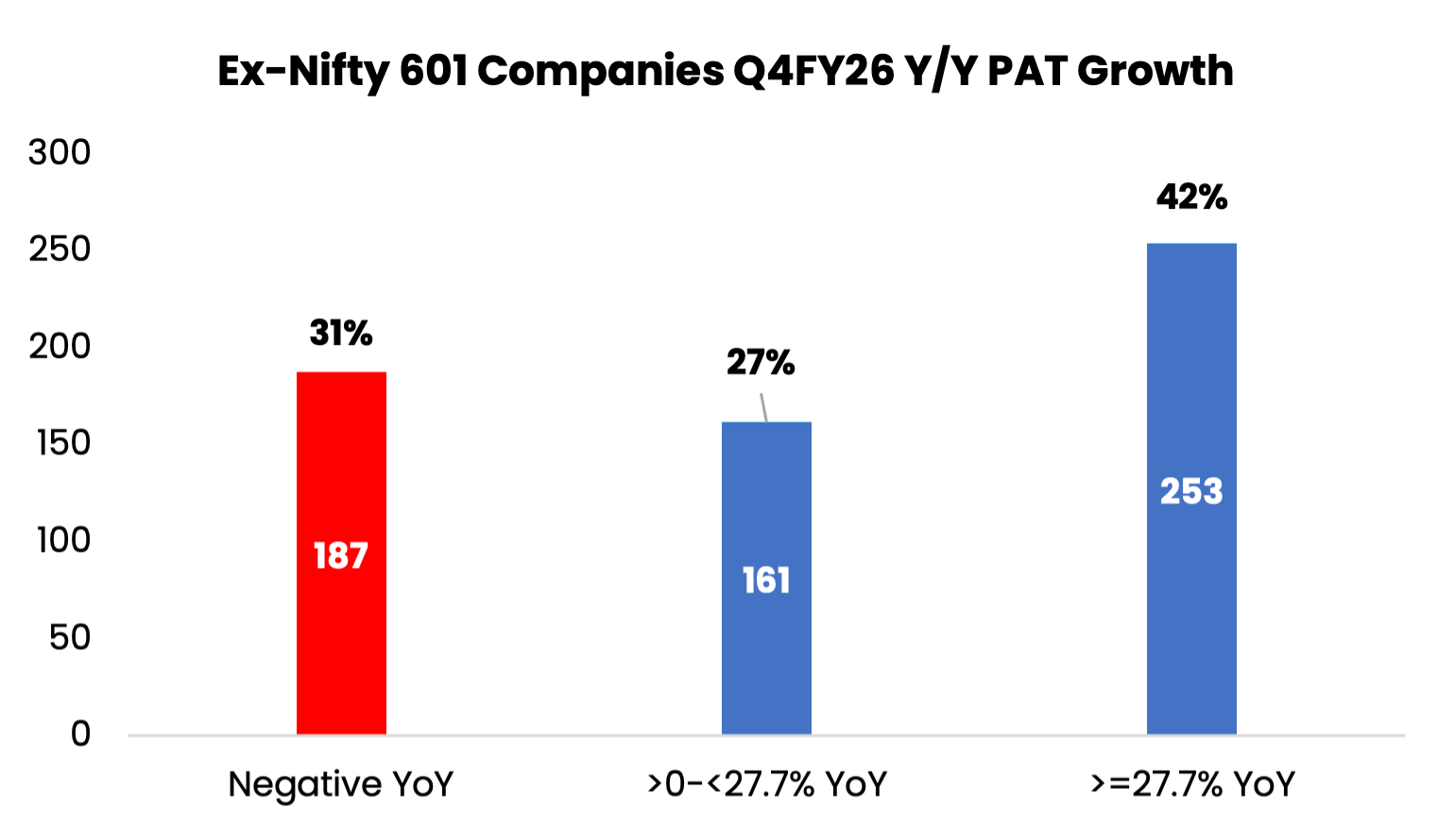

For Q4 FY26, a selected basket of 601 companies (excluding Nifty 50) recorded an aggregate net profit growth of ~27.7% YoY and ~22.4% QoQ. Within this group, notably, 42% (~253 companies) delivered profit growth exceeding 27.7% (y/y), indicating a strong skew towards high-growth performers. For full financial year FY’26 same set of companies delivered ~20% net profit growth (y/y). Earnings growth was largely driven by mid-cap companies (MCap ranking 51 to 200).

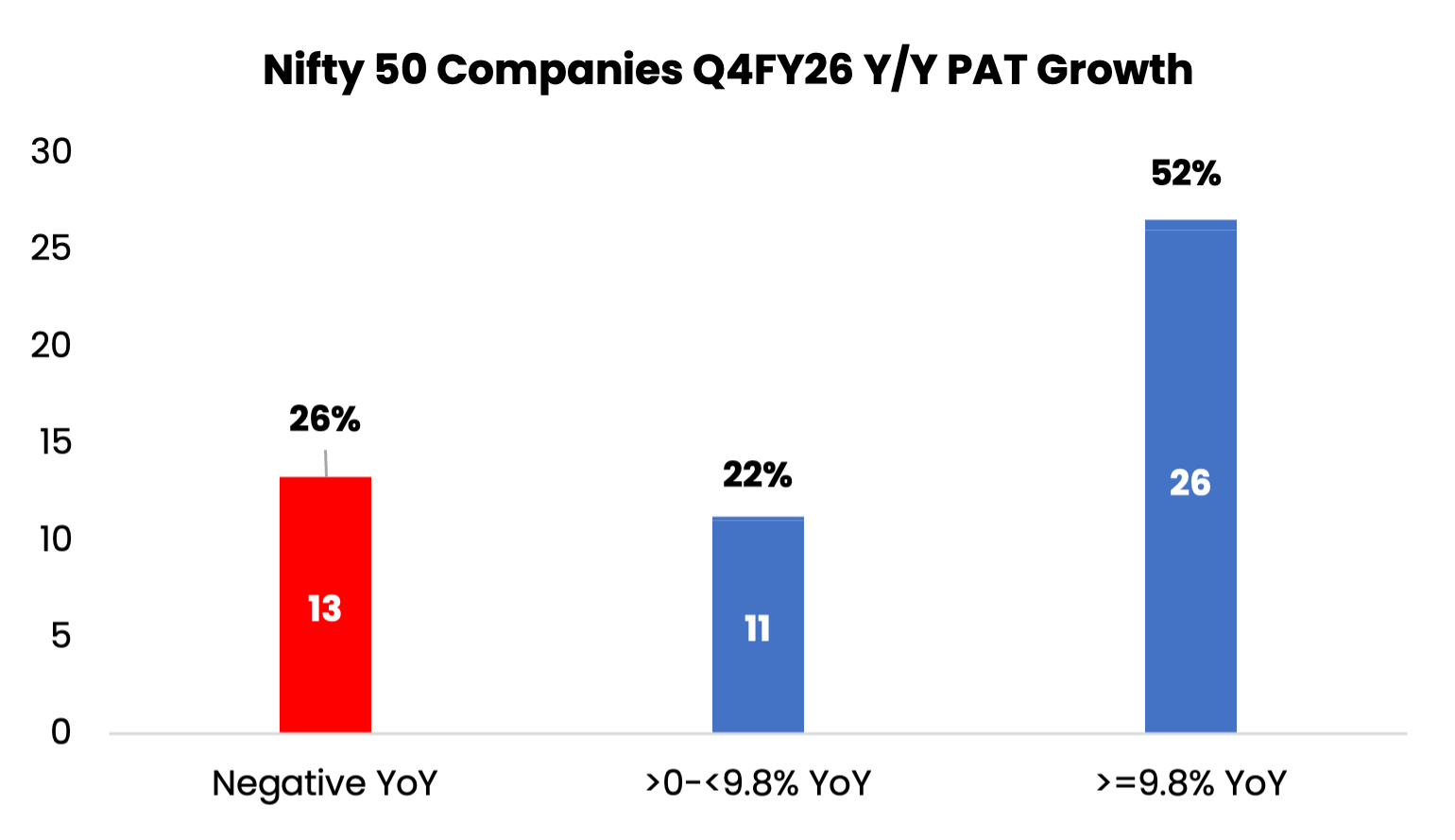

Similar analysis for Nifty 50 companies for FY26 on proforma PAT basis (excluding gains from select companies such as JSW Steel, Tata Motors (PV), Hindustan Unilever and Reliance Industries), reflects moderation in profit growth to ~3.72% YoY.

Sectoral performance remained divergent yet constructive overall, with industrial products, metals, automobiles and auto ancillaries, cement, healthcare, power, capital goods and defense emerged as key outperformers, where tailwinds of direct and indirect tax cuts and interest rate cuts played out. Higher infrastructure spending by government led to domestic capex revival and strong execution.

Among financials NBFCs, HFCs, Public sector banks delivered AUM and net profit growth in the range of high teens to mid-twenties while large private sector banks lagged. However, remarkably internals like asset quality, fresh slippage, credit cost indicated strong underlying economic momentum.

Struggle for IT services companies particularly large ones like Infosys, TCS, Wipro, HCL tech continues, partially negated by INR depreciation. Business model of these companies with respect to AI disruption is yet to be demonstrated and whether it can be a growth driver or a sustainability mechanism.

Source: CSEC Research, Bloomberg, NSE, BSE, Corporate Filings • Date: 3rd June, 2026

In FY’26 headwinds came from fluctuating US tariffs which was effectively tackled by policy measures taken by Indian Government and regulators, namely direct and indirect tax rate cuts along with interest rate cuts by RBI.

GST rate cuts did boost consumption across the board. Sharp volume growth was seen in automobile sales, FMCG consumption, tourism and hotels, Jewelry, Apparels and Realty. Which is now challenged by supply disruption led rising inflation and prospects of deeper monsoon rainfall deficit.

Inflation remains a key concern. Commodity prices remain at elevated levels while series of fuel price hikes are rolling in. RBI’s CPI inflation tolerance band of 4–6% is under challenge. Though in all likelihood growth will be a priority for RBI and monetary policy will revolve around it.

Additional concerns stem from monsoon uncertainties, with forecasts indicating below-normal rainfall alongside ongoing heatwave conditions. These factors raise the risk of renewed food inflation and rural demand softness, potentially impacting broader economic momentum.

INR depreciation is the biggest concern. It’s a double whammy on back drop of elevate commodity and crude oil prices, India being net importers.

Best case scenario will be resolution of West Asia crisis by June end. In the event of it happening, we see :

1st half of FY’27 delivering negative earnings growth for corporate India. Operating margins will come under pressure on higher input cost and insufficient price hikes. There seems to be a consensus in management commentaries where keeping volume growth on track will be priority.

Most of catch will happen in 2nd half of FY’27 with onset of festive season, probably policy measures by Government to reign in INR depreciation and commencement of cool off in commodity prices.

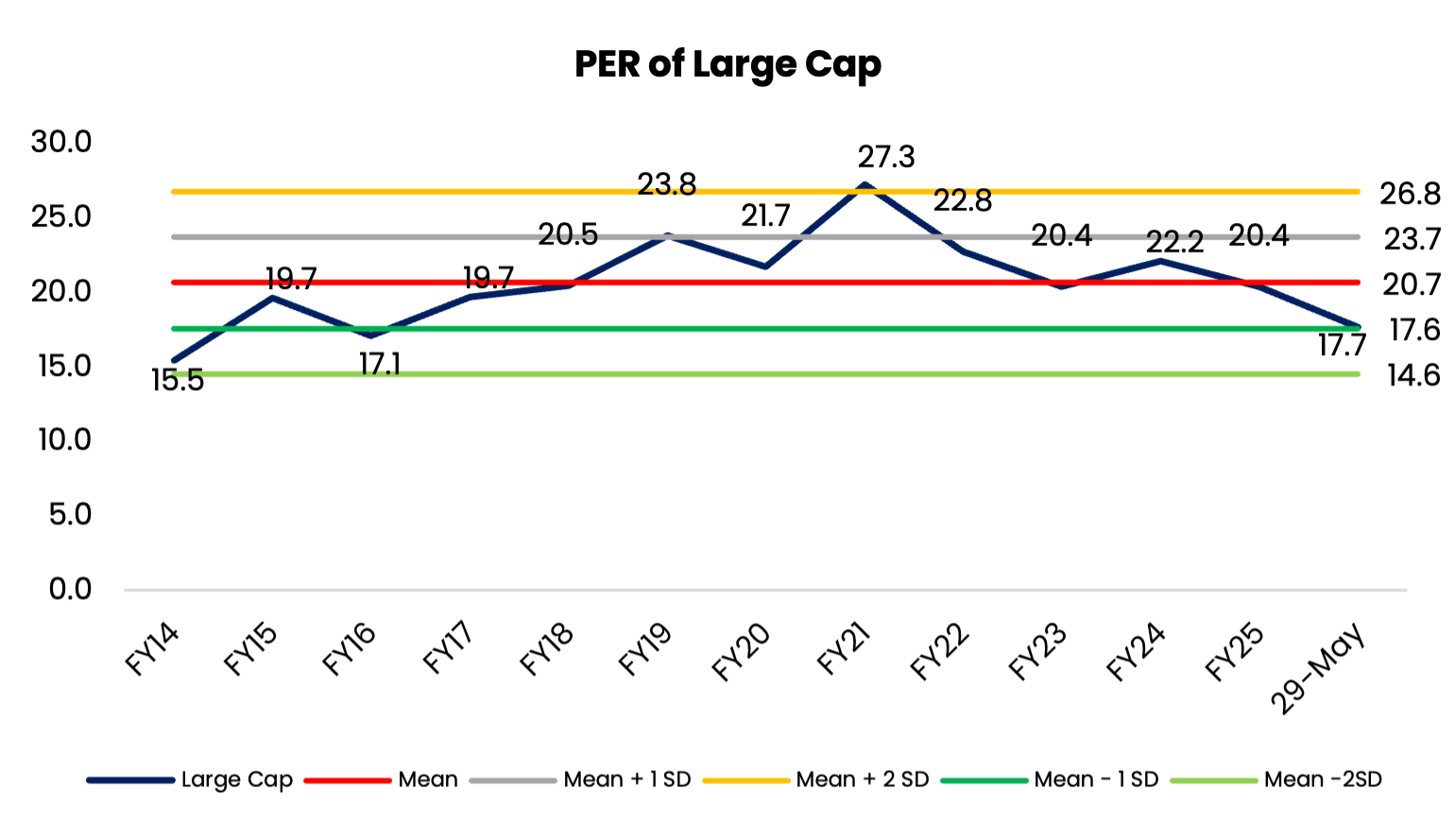

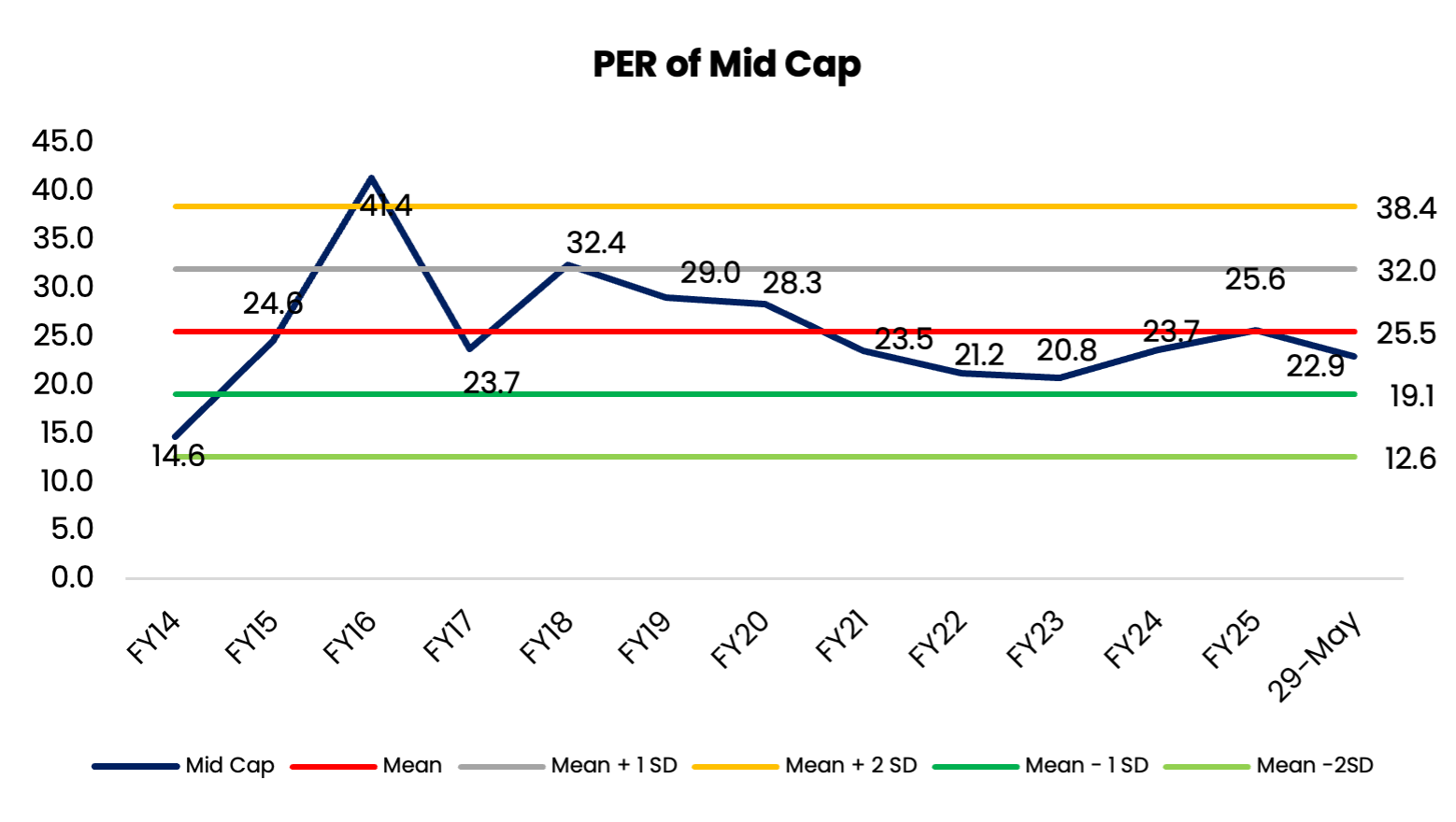

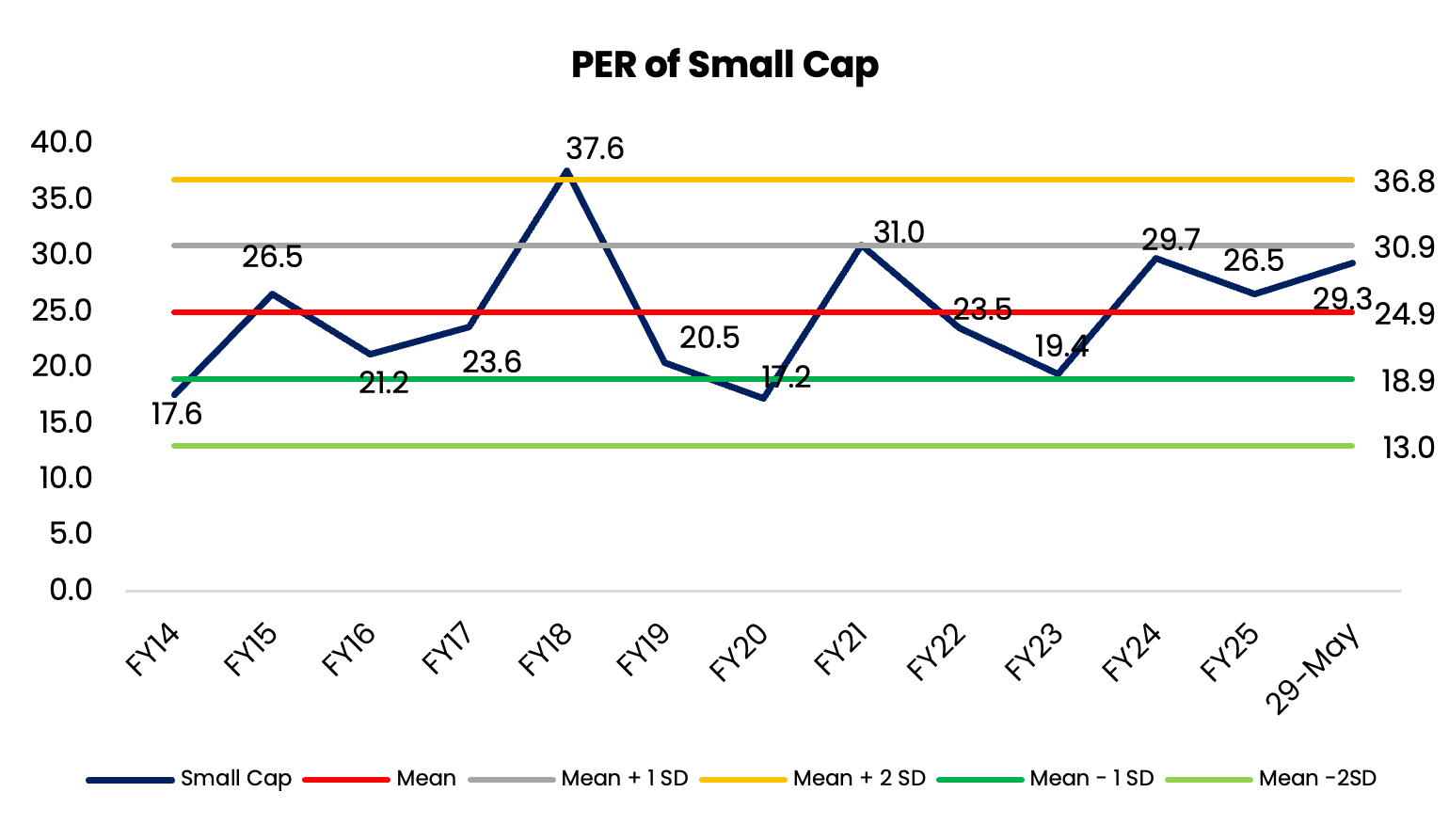

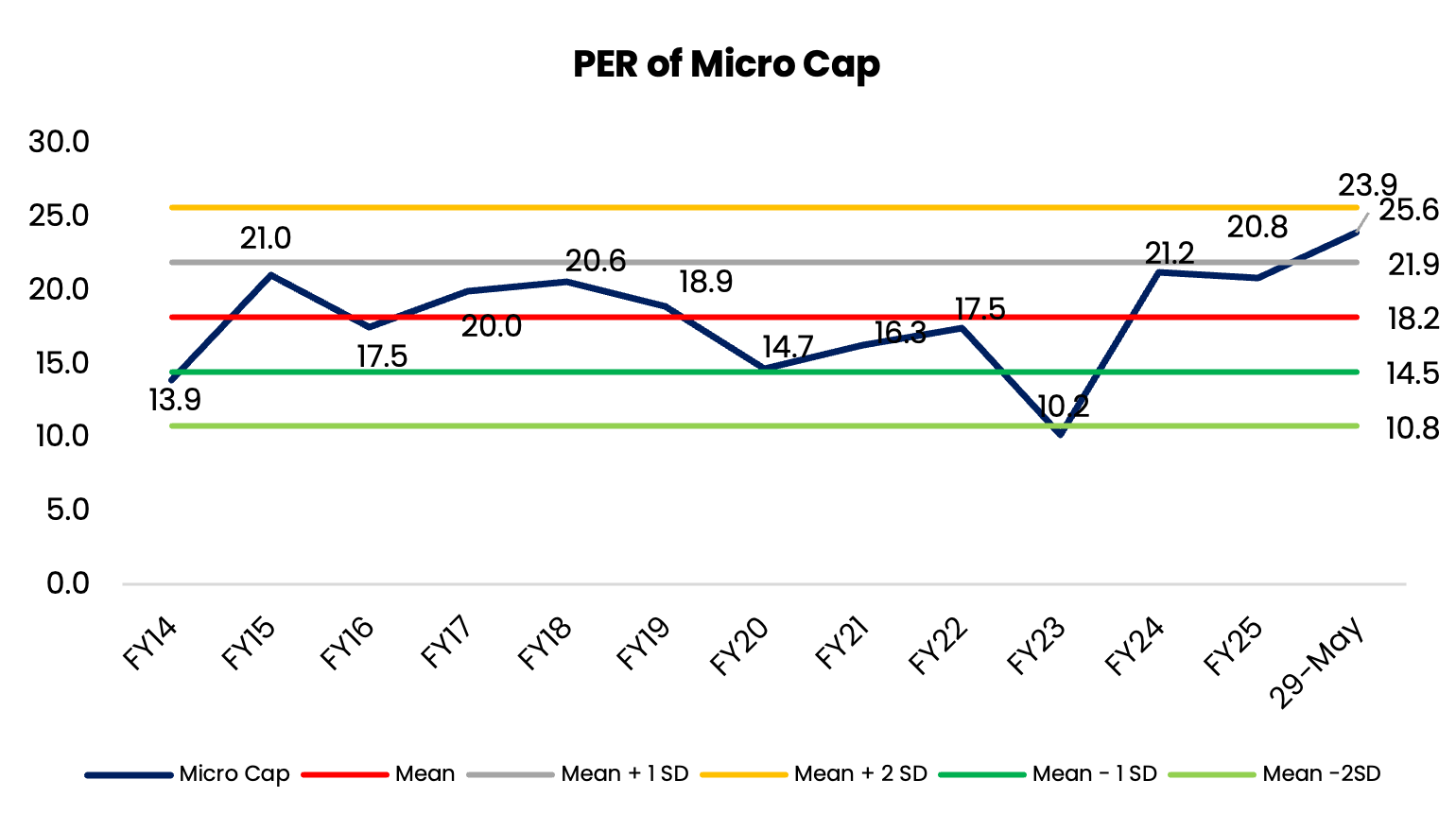

If by June end US and Iran reaches an agreement on opening Strait of Hormuz, market will be in for a fiery up move. While the cool off in commodity prices will happen over next 6 months in tandem with poor earnings reporting by corporates for Q1 and Q2 but due to forward looking nature of market it will be scaling up aided by valuation comfort as large and mid caps are trading near -1 SD from mean multiples of PER on TTM basis .

Overall, FY’27 is likely to deliver low to mid single digit earnings growth for Nifty’50.

Source: CSEC Research, Bloomberg, NSE, BSE, Corporate Filings • Date: 3rd June, 2026

(Proprietary grouping of NSE 500)

Large Cap

Top 50 Stocks (1–50)

Mid Cap

Next 150 Stocks (51–200)

Small Cap

Next 250 Stocks (201–450)

Micro Cap

Last 50 Stocks (451–500)

Universe

Proprietary grouping of NSE 500 stocks

Source: CSEC Research, Bloomberg, NSE, BSE, Corporate Filings • Date: 3rd June, 2026

(Proprietary grouping of NSE 500)

PE as on 29/05/26 calculated with FY26 PAT

Source: CSEC Research, Bloomberg, NSE, BSE, Corporate Filings • Date: 3rd June, 2026

PAT Summary

| Sr No | Particulars | Q4FY26 | Q3FY26 | Q4FY25 | Y/Y% | Q/Q% | FY26 | FY25 | Y/Y% |

|---|---|---|---|---|---|---|---|---|---|

| 1 | PAT | 5,31,189 | 4,36,924 | 4,49,660 | 18.13% | 21.57% | 18,83,188 | 16,02,346 | 17.53% |

| Sr No | Particulars | Q4FY26 | Q3FY26 | Q4FY25 | Y/Y% | Q/Q% | FY26 | FY25 | Y/Y% |

|---|---|---|---|---|---|---|---|---|---|

| 1 | PAT | 2,67,803 | 2,18,827 | 2,09,753 | 27.68% | 22.38% | 8,74,408 | 7,28,033 | 20.11% |

| Sr No | Particulars | Q4FY26 | Q3FY26 | Q4FY25 | Y/Y% | Q/Q% | FY26 | FY25 | Y/Y% |

|---|---|---|---|---|---|---|---|---|---|

| 1 | PAT | 1,56,775 | 1,45,718 | 1,35,901 | 15.36% | 7.59% | 5,74,051 | 5,33,025 | 7.70% |

| Sr No | Particulars | Q4FY26 | Q3FY26 | Q4FY25 | Y/Y% | Q/Q% | FY26 | FY25 | Y/Y% |

|---|---|---|---|---|---|---|---|---|---|

| 1 | PAT | 38,995 | 31,039 | 34,404 | 13.35% | 25.63% | 1,37,273 | 1,31,425 | 4.45% |

| Sr No | Particulars | Q4FY26 | Q3FY26 | Q4FY25 | Y/Y% | Q/Q% | FY26 | FY25 | Y/Y% |

|---|---|---|---|---|---|---|---|---|---|

| 1 | PAT | 2,63,386 | 2,18,098 | 2,39,907 | 9.79% | 20.77% | 10,08,780 | 8,74,313 | 15.38% |

Source: CSEC Research, Bloomberg, NSE, BSE, Corporate Filings • Date: 3rd June, 2026

Source: CSEC Research, Bloomberg, NSE, BSE, Corporate Filings • Date: 3rd June, 2026

(Q4FY26 Earnings Wrap Up)

During the quarter, the sector saw a stable demand in India, reflecting consumption resilience backed by fiscal measures of direct and indirect tax rationalization. Rural markets continued to outperform urban markets, although gap between urban and rural has narrowed. Additionally, the companies also benefitted from pricing actions, premium product launches and increased distribution reach. However, the geopolitical headwinds in the Middle East are impacting input costs and supply chain across businesses, including India. Moving ahead, the industry volume growth could softened, due to persistent elevated crude oil prices arising from West Asia crisis and the risk of a below-normal monsoon, which may lead to higher food inflation and exert pressure on consumption and margins.

In the liquor sector, IMFL growth was driven by premiumization, while mass‑segment demand was temporarily impacted by changes in policy in Maharashtra and Karnataka; While, the beer segment saw recovery in the demand, supported by favorable policy environment, wherein the taxes will be levied as per the alcohol content which effected price reduction for beer improving affordability.

The consolidated revenue grew by +8.84% YoY, while PAT grew by +13.94% YoY. The operating margins for the quarter were 22.57%, reflecting an improvement of 76 bps YoY and 113 bps sequentially.

HUL: The company reported a consolidated Underlying Sales Growth (USG) of 7% and an Underlying Volume Growth (UVG) of 6%. Home Care delivered 9% USG, driven by high-single digit UVG; Beauty & Wellbeing delivered 8% USG with mid-single digit UVG; Personal Care USG grew 5%; Foods delivered 5% USG with high-single digit UVG.

Tata Consumer Products: The consolidated revenue from operations grew by 17.91%, driven by underlying volume growth of 16% in the Branded Business. The India business recorded 13% growth. The International Business continued its momentum with a 11% constant currency revenue growth, led by the US Coffee business. During FY26, Tata Starbucks added 23 net new stores, including new store formats, bringing the total number of stores to 502 across 80 cities.

Varun Beverages: Consolidated sales volume grew by 16.3% to 363 million cases in Q1CY26 from 312 million cases in Q1CY25, Sales volumes in India was 260 mn cases and international markets was 103 mn cases. The product mix for Q1CY26 constituted: CSD: 74%, NCB: 7%, and Packaged Drinking Water at 19%. Consolidated improved realizations in international territories primarily due to favourable currency movement. During the quarter, the company consummated the acquisition of Twizza in South Africa. Additionally, the company has also entered into an agreement to acquire Crickley Dairy Proprietary Limited. The acquisition is expected to be completed on or before 30 June 2026.

Radico Khaitan: The company delivered a strong performance in Q4FY26, as the consolidated revenue grew by +15.31%, driven by an improved premium mix and robust consumer demand, while the margin expansion was driven by a premium-led portfolio, a stable raw material environment and enhanced operating leverage. The Prestige & Above (P&A) segment recorded a notable 27.9% YoY volume increase, while the regular segment declined on YoY basis was due to a higher base of Q4FY25 after the change in the route-to-market in the state of Andhra Pradesh, and the impact of the policy change in Maharashtra and Karnataka.

The overall performance for consumer durable was subdued impacted by the global macro landscape arising from geopolitical tension due to US-Iran war, escalated disruption in supply chains, freight costs, energy prices, and currency movements.

As a result the input cost remained elevated majorly in the smartphone and IT hardware segment. Additionally, the rapid growth of AI has resulted in elevated prices in key components likes memory chips and semiconductor due to supply constraints. Further, the air cooling categories saw weaker initial traction as a milder start to the summer season impacted channel stocking.

The companies saw a growth of 27.86% YoY in revenue, while PAT grew by 43.56% YoY. The operating margin for the quarter came to 9.76%, a decline of 61 bps Y/Y and 81 bps Q/Q.

Blue Star: The company’s revenue grew marginally by 1.32% YoY, with electromechanical projects & packaged AC (EMP) growing at 1.11% YoY, while Unitary products grew by 1.26% YoY. Rising opportunities in data centers and factories giving confidence of continued growth prospects. The order inflows in Commercial Air Conditioning Systems gained momentum during the quarter, supported by demand from government, industrial and retail segments. Additionally, RAC segment saw a reasonable growth as primary demand picked up in March for summer stocking.

Dixon Technologies: During Q4 FY26, revenues remained stable, supported by stable demand from key clients. However, profitability was impacted by higher input costs, elevated memory prices, and product mix changes, which exerted pressure on margins. Backward integration under the HKC joint venture is expected to commence in Q3 and Q4 of the financial year, which is likely to help ease elevated margin pressures. Further, the company has received PN3 approval for the display module in partnership with HKC, marking a key milestone in strengthening its component manufacturing capabilities. This approval enables the joint venture to scale up local production of display modules, enhancing value addition and reducing dependence on imports.

The auto ancillary segment showed positive traction in operating margins, which stood at ~13.49%, expanding by ~79 bps YoY and ~22 bps QoQ, supported by operating leverage and better product mix.

Wholesale volumes witnessed healthy growth across M&HCVs, tractors, and passenger vehicles, driving strong demand for auto components. The domestic business remained robust, supported by sustained automotive demand, replacement cycles, and improving rural sentiment.

The near-term outlook remains cautiously positive, supported by continued capacity expansion, diversification across EV and premium segments, and strong OEM demand.

Revenue growth was 18.28% YoY and 7.39% QoQ while PAT improved 23.27% YoY, 17.28% QoQ. The sector’s performance remained robust, largely driven by healthy demand trends in the automotive segment.

Export markets, particularly in the US, showed gradual recovery, supported by replacement demand arising from an ageing commercial vehicle fleet. Electrification continued to remain a key structural theme, with BEV adoption gaining traction across both the US and Europe.

Commodity inflation remained elevated, particularly in key raw materials such as aluminum and copper. Additionally, higher energy costs and increased freight and shipping expenses exerted pressure on margins.

The tyre industry enjoyed strong domestic demand across both OEM and replacement categories. Domestic demand remained strong while international business is seeing signs of recovery, particularly in Commercial vehicles in the US and Europe. Rubber prices and rupee depreciation have led to a spike in raw material prices putting pressure on pricing across segments, with further increases expected in the next quarter.

The combined sales of the companies under review grew +17.9% YoY and +3.03% QoQ in Q4 FY26, supported by robust performance across passenger vehicles and commercial vehicles, aided by improved consumer sentiment, and recovery in demand across segments.

Q4 FY26 witnessed widespread growth across domestic and export markets, supported by festive demand (with Navratri falling in March), rural recovery, infrastructure push, and stable interest rates.

The sector witnessed a 16.3% YoY improvement in revenue during the quarter, while PAT declined by 5.4% YoY, impacted by higher commodity prices.

Domestic vehicle sales witnessed ~10.4% YoY growth during FY26 to ~2.82 crore units, supported by recovery in both urban and rural demand.

Passenger vehicle sales surged to all-time highs, rising ~7.9% YoY to ~46.4 lakh units, with Maruti Suzuki, Tata Motors, and Mahindra & Mahindra leading growth, reflecting strong consumer sentiment and robust product acceptance across segments.

SUVs accounted for ~65–67% of total PV volumes, highlighting sustained preference for larger, feature-rich models, while hatchbacks and entry-level cars saw relatively moderate traction.

Commercial vehicle sales reported healthy growth (~12.6% YoY to ~10.8 lakh units), led by strong demand in MHCVs driven by infrastructure, mining, and industrial activity, while farm equipment and agri-machinery segments also maintained firm momentum, supported by rural liquidity and post-harvest demand.

Exports for PV remained gradual and selective, while CV exports showed a stronger recovery led by replacement demand, with overall trends improving but still uneven across geographies.

The combined sales of the companies under review grew 24.6% YoY and 1.2% sequentially, supported by strong performance across the board.

Margins witnessed some pressure during the quarter, primarily due to higher raw material costs and elevated commodity prices, which partially offset gains from operating leverage and calibrated price hikes. The margins stood at 15.71%, decline of 42 bps YoY & 213 bps QoQ.

Q4 FY26 saw broad-based growth across urban, rural, and export markets, with festive demand on the back of Navratri and stable interest rates driving retail momentum. Favorable policy support for electric mobility further boosted demand, with electric two-wheelers gaining market share.

The consolidated revenue growth of ~31.2% YoY and PAT surge of ~70.8% YoY for the companies under review are consistent with reported financials.

The domestic two-wheeler segment recorded a strong performance in Q4 FY26, with total sales rising ~26.4% YoY to ~5.77 million units, marking the highest-ever quarterly volumes for the industry.

The segment delivered a strong and stable performance, closing the year on a high supported by robust domestic demand and improving export traction.

Motorcycles and scooters both recorded steady growth, with premium and commuter segments benefiting from new launches and improved rural sentiment, while scooters continued to gain traction in urban markets.

Electric two-wheelers maintained strong adoption momentum, supported by government incentives, an expanding ecosystem, and increasing consumer acceptance.

Exports registered healthy growth, led by demand from Africa, Latin America, and South Asia, with Indian OEMs benefiting from favorable currency dynamics and competitive positioning.

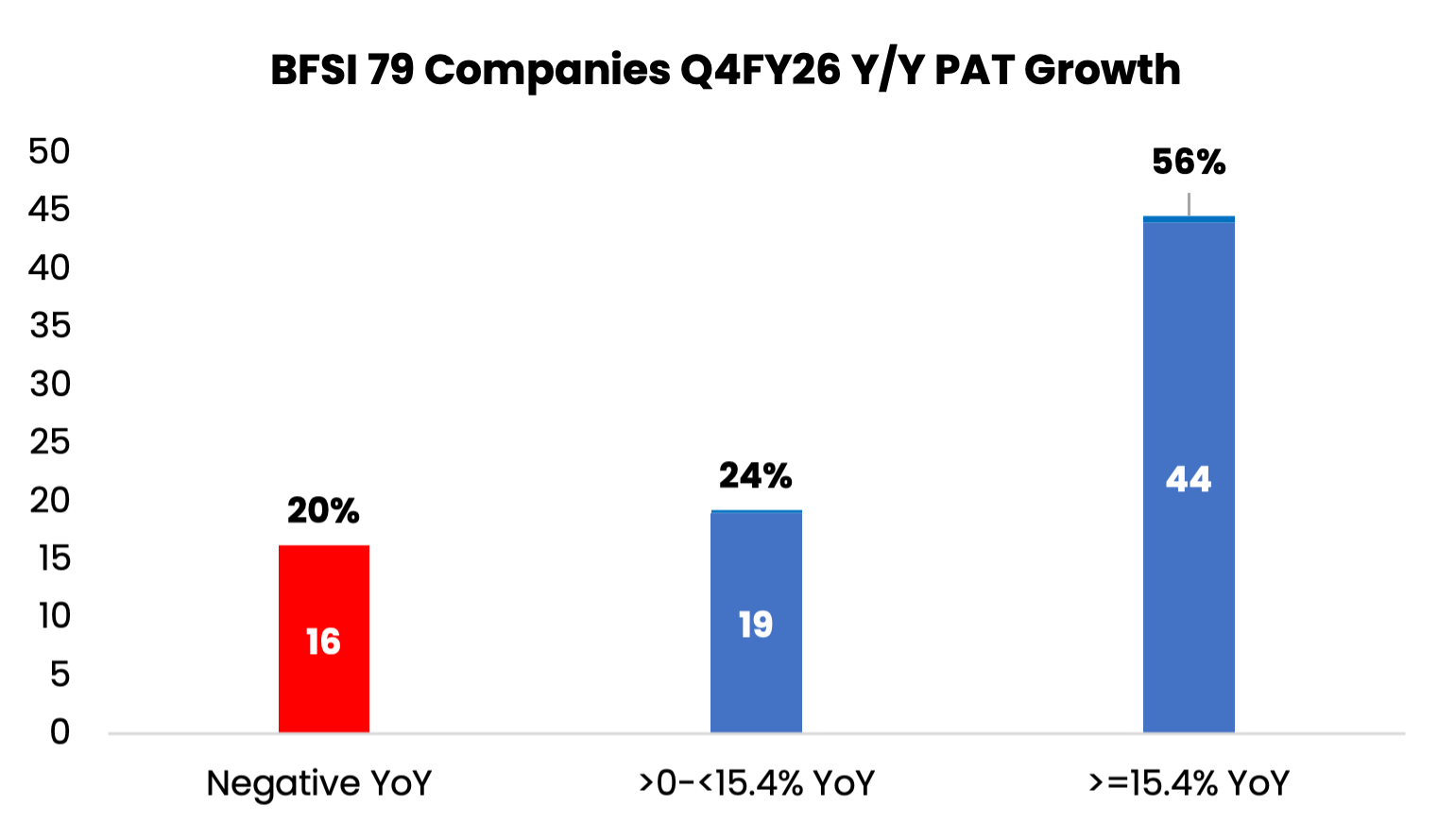

Private sector banks delivered a resilient performance in Q4 FY26 and FY26, characterized by steady growth, improving asset quality, lower provisioning and moderating credit costs.

Credit growth remained healthy and strong across the year, with the average advances growth for the 8 banks under review at ~15.7% YoY, reflecting sustained demand across retail, MSME, and corporate segments. On the liabilities side, deposit growth remained robust but slightly lagged credit growth, with the average deposits growth for these banks at ~14.35% YoY. The continued gap between credit and deposit growth led to elevated credit-deposit ratios and ongoing pressure on funding costs.

Profitability showed stable recovery and gradual improvement, as the banks reported high single-digit growth in PAT in Q4 FY26, supported by lower provisioning and stable operating performance.

| Company Name | Advances (YoY%) | Deposits (YoY%) |

|---|---|---|

| Axis Bank | 18.50% | 13.90% |

| ICICI Bank | 15.80% | 11.40% |

| YES Bank | 11.10% | 12.10% |

| Federal Bank | 14.40% | 10.60% |

| IDFC First Bank | 20.00% | 16.80% |

| Kotak Mahindra Bank | 16.20% | 14.70% |

| HDFC Bank | 11.97% | 14.40% |

| DCB Bank | 17.60% | 20.90% |

Public sector banks delivered a strong performance in Q4 FY26, supported by strong credit growth, continued improvement in asset quality, and steady profitability, even as liability-side pressure persisted.

Margins remained broadly stable after earlier compression, aided by better yields and near completion of deposit repricing.

Advances continued to outpace deposit growth, reflecting strong credit demand. The average advances growth for the 8 banks under review stood at ~15.2% YoY, while deposits grew at a relatively lower ~10.32% YoY. The growth mix remained well-diversified, with momentum across retail, agriculture, and MSME segments, alongside a gradual pickup in corporate lending.

| Company Name | Advances (YoY%) | Deposits (YoY%) |

|---|---|---|

| State Bank of India | 16.80% | 11.00% |

| PNB | 12.70% | 9.22% |

| Indian Bank | 13.40% | 12.30% |

| Union Bank of India | 9.70% | 2.70% |

| Bank of Baroda | 16.20% | 12.00% |

| Canara Bank | 15.30% | 7.70% |

| Bank of Maharashtra | 21.70% | 14.10% |

| Bank of India | 15.80% | 13.50% |

The sector delivered a mixed but resilient performance in Q4 FY26, supported by continued credit demand and segment-specific growth, although profitability and asset quality trends varied across lenders.

NBFC’s maintained steady loan growth, driven primarily by retail-focused segments such as vehicle finance, gold loans, and affordable housing, while select corporate-focused NBFCs also saw gradual recovery.

AUM growth remained robust across most segments, supported by improving economic activity and demand revival.

| Company Name | AUM (YoY%) | Asset Quality |

|---|---|---|

| Bajaj Finance | 22.40% | Asset quality improved |

| Poonawalla Fincorp | 69.40% | Asset quality improved |

| Aadhar Housing Finance | 19.74% | Asset quality improved |

The consolidated operating margin for the quarter stood at 19.67%, reflecting an improvement of 294 bps YoY and 25 bps QoQ.

Exports during Q4 FY26 remained robust and widespread, with double-digit growth across cables, engineering goods, EMS, and renewables, supported by China+1 tailwinds, strong demand from emerging markets, and a competitive cost advantage for Indian manufacturers, although margins were partly impacted by input cost pressures and execution mix.

On a consolidated basis, the companies delivered 53.05% YoY revenue growth, while PAT increased by 60.9% YoY.

The broader industrial products and electricals industry recorded a robust financial performance in Q4 FY26 and FY26, largely driven by the ongoing domestic infrastructure capex cycle, strong demand for commercial and industrial cables, and an unprecedented surge in renewable (solar) and defence investments.

FY26 marked a structural upcycle year, with H2 significantly stronger than H1 across most industrial segments.

The wires, cables, and electricals segment reported strong double-digit revenue growth, supported by healthy volume expansion, while the FMEG segment also witnessed sharp acceleration, driven by improving consumer demand and product mix.

The quarter was a standout for the renewable energy and solar segment, with higher operational efficiencies and capacity utilization leading to multi-fold growth in profitability.

Most companies in the segment recorded robust order book growth driven by orders across building & infrastructure, transport, renewables, data centres and T&D.

Despite the strong growth in order book, managements flagged the risk of margin compression due to the ongoing tensions in the Middle East with spillover expected to extend to Q3FY27, if the situation prolonged.

The sectors’ operating margins for the quarter came at 14.69%, an improvement of over 149 bps Y/Y.

The companies witnessed growth of 26.32% Y/Y in revenue, along with a 33.2% Y/Y increase in PAT, driven by the execution of strong order backlogs.

Companies remained bullish on transmission & distribution business citing increasing intermittency, long-distance evacuation needs, and higher system complexity—supporting HVDC, digital/grid solutions, and high-voltage equipment demand.

Momentum within the infrastructure sector for the quarter remained negative on a yearly basis but a signs of gradual improvement across multiple verticals on sequential basis. The impact was largely operational, stemming from external factors that temporarily slowed execution.

However, the sector was defined by a massive surge in government project announcements and robust order inflows. The new project added in Q4FY26 was 483 (vs 38 projects in Q4FY25), led by highways.

According to MoSPI, the total cost of projects added during Q4 FY26 stood at Rs. 6.01 lakh crores, up +544.9% YoY from Rs. 93,213 crore in Q4FY25 providing strong execution runway.

The companies’ revenue performance for the quarter declined by 3.12% YoY with PAT declining by 1.12% on YoY basis.

Operating margins decline by 55 bps YoY and 94 bps QoQ, settling at 11.33%.

NCC Ltd: Order book as on 31 March 2026 was Rs 83,004 Crores registering a growth of +16% YoY. Buildings accounted for 27% of order book, transportation 20%, mining 18%, water & railways 12%, Electrical (T&D) 17% and irrigation and others the balance 6%. NCC recorded a fresh order inflow of Rs 9,573 crores during Q4FY26.

KEC International: Order book as on 31 March 2026 is Rs 36,267 crores which was +8.6% YoY. The company achieved an order inflow of Rs 25,280 Crores in FY26. Current Order book + L1 stood at Rs. 40,000+ crores, with T&D contributing the maximum of ~62%, followed by Civil (26%), Transportation at 6%, Cables at 3%, Renewables at 2% and Oil & Gas at 1%.

The operating margin for the quarter stood at 23.37%, reflecting an improvement of 217 basis points YoY but a decline of 7 bps QoQ.

Overall, in Q4FY26 the segment delivered +10.57% revenue growth YoY, while PAT grew by +17.41% YoY.

Government defence and shipbuilding capex remained a key growth catalyst. Key ongoing projects include: Project 17A (Stealth Frigates), Project 15B (Destroyers), and Project 75(I) (Submarines), along with firm orders for LCA Tejas Mk-1A and HTT-40 Trainers; and the Ministry of Defence’s FY26 capital acquisition budget of ~Rs. 1.72 lakh crore, which continues to underpin visibility for these companies.

Several mid-cap defence and EMS companies highlighted encouraging international demand and global sourcing mandates during Q4FY26, driven by the ongoing global supply-chain diversification and rising demand for high-reliability electronics, subsystems, and precision-engineered components.

Hindustan Aeronautics Ltd: During the year, the fresh orders received by the company were Rs 97,028 crores, which includes the manufacturing orders of Rs 69,668 crores and ROH orders of Rs 26,539 crores. Major orders bagged include contracts for the supply of 97 LCA Mark-1A to IAF, quantity 6 ALH Mark III MR to ICG, quantity 8 Do-228 to ICG, quantity 10 ALH Dhruv NG to Pawan Hans, quantity 2 Hindustan-228 to Guyana. Management also highlighted promising order pipeline with additional anticipated contracts of 143 ALH for the Army, IAF Su-30 upgrade, upgrade of 40 Do-228, etc., are at various stages of approval. In total, we expect to receive orders of Rs 90,000 crores, including the ROH orders, during the next 2 years.

Bharat Electronics Ltd (BEL): As of 1 April 2026, BEL’s order-book stood at Rs. 73,882 crore, +3% YoY and +1% QoQ. Order intake for the full year FY26 stood at Rs 30,045 crores, achieving its FY26 guidance. For FY27, the management anticipates order inflows to reach a staggering Rs 55, 000 crores (excluding QRSAM).

Companies reported low single digit revenue growth in CC terms. However, in INR terms , topline growth ranged between high single digit and double digit growth aided by currency tailwinds.

Looking ahead, revenue guidance for FY27 was in the lower single digits in CC terms as managements cited challenging macro environment, delayed project ramp ups and AI related deflation.

AI has become productized and commercialized with all major IT services companies outlining strategies to capture the large scale AI tailwinds.

The companies recorded a low double digit YoY revenue growth in Q4FY26 with PAT growth at 13.35% YoY.

Operating margins improved marginally by 47 bps YoY and 31 bps QoQ, settling at 19.73%, largely on account of currency translation tailwinds.

Infosys reported large deal wins totaling $3.2 billion for Q4FY26, +23.08% YoY and -33.33% QoQ. HCL Tech’s TCV (New Deal Wins) were $3Bn, -37% YoY and QoQ. Persistent Systems recorded total contract value (TCV) of $600.8 million, +16.1% YoY and -10.93% QoQ. Wipro closed the quarter with total bookings of $3.5 billion, -13.9% YoY and +3.2% sequentially; the company’s large deal bookings were at $1.4 billion. LTM Ltd (formerly LTI Mindtree Ltd) reported total order inflows of $1.7 Bn, up +6.25% YoY and flat QoQ and marking the sixth consecutive quarter of orders inflows >1.5bn.

For FY27, Infosys guided revenue growth of 1.5-3.5%; operating-margin band has been maintained at 20 – 22 %. HCL Technologies guided revenue growth of 1-4%. EBIT margin is expected to be between 17.5% - 18.5% for HCL. Wipro guided for Q1FY27 IT-services revenue growth of -2% to 0% (CC).

Total power demand for the country grew modestly at 0.9% in FY26, the most muted growth in last five years, driven by an extended monsoon season that weighed on consumption through the first half of the year.

However, Q4FY26 saw the onset of power demand recovery, with demand growth rebounding to 2.2%.

In FY27, for the first two months, the YTD demand growth remains healthy at a growth of 4.6% YoY.

Companies in the sector reported a 4.65% YoY increase in revenue, while PAT saw a +24.57% YoY growth. Major contributors to aggregate. The surge in PAT growth was largely on account of deferred taxes amounting to Rs 10,311 crores recognized by NTPC Ltd.

Operating margins for the sector stood at 34.41%, reflecting a flat performance on YoY basis and a decline of 206 bps QoQ.

India added 64.9 GW of new capacity during FY26, of which renewable energy accounted for 50.9 GW, translating to 78% of total capacity additions.

FY26 was a landmark year with non-fossil sources crossing 50 per cent of total installed capacity for the first time.

The merchant market remained soft through most of FY2026, averaging approximately ₹3.86 per unit on exchanges, reflecting muted demand.

Steel consumption in Q4 stood at 44.6 million tonnes (MT), registering a growth of 11% YoY and 10% sequentially. India was a net exporter at 0.1 MT. Strong Q3 and Q4 exports along with a decline in imports aided by safeguards by GoI helped India turn next exporter in FY26 after two years of net imports.

India’s copper demand at 402 kt (+5% YoY and -5% QoQ) with YoY growth driven by demand across building & consturction segment.

Meanwhile, aluminium demand reached 1,561 kt (+9% YoY and flat QoQ), with YoY growth primarily driven by strong demand in Auto & Electricals.

The companies saw a 16.14% YoY improvement in revenue, while PAT grew by 75.47% YoY. Operating margins stood at 19.10%, an improvement of 126 bps YoY and 204 bps QoQ. The YoY surge in PAT was largely on account of exceptional items recognized by JSW Steel on account of BPSL slump sale.

JSW Steel: The consolidated steel production for Q3FY26 stood at 7.49 MT, down 2% YoY, while sales was at 7.97 MT, up 6% YoY, primarily driven by strong domestic demand.

Hindalco: Aluminium shipments at Novelis, its international subsidiary, declined by 12% YoY to 844 kt, with volumes impacted largely by fire incident at its New York plant. However, in India, upstream aluminium shipments rose 2% to 339 kt while downstream aluminium shipments jumped by 18% to 124 KT on the back of healthy domestic demand. Copper shipments declined by -5% to 128 KT while CCR (Continuous Cast Copper Rods) shipments declined -17% YoY to 91 KT.

Hindustan Zinc: The company recorded its best ever mined metal and refined metal production in Q4FY26 at 315 kt (+2% YoY) and 282 kt (+4% YoY). Revenues improved 49.05% YoY amidst improving commodity prices , especially silver which was up 165% YoY. EBITDA margins improved 385 bps to 56.90% aided by improved commodity prices and continued improvements in cost of production.

The secondary sales as per IQVIA during the quarter was 8.7% versus 10.7% IPM, excluding GLP-1, primarily due to strong performance in chronic growth supported by 14.7% in cardiac and 11.6% in anti-diabetes; muted growth in anti-infective, partially offset by QoQ recovery in gastro, gynec, vitamins and derma.

The Indian pharmaceutical sector is witnessing a trend where companies are aggressively acquiring brands and expanding. On 21st Jan 2026, Torrent Pharmaceuticals successfully completed its acquisition of a controlling stake in JB Chemicals & Pharmaceuticals by purchasing a 46.39% stake.

The recent quarter witnessed a steady revenue growth but the margins continued to remain under pressure.

Consolidated revenue grew by +9.06% YoY and +1.54% QoQ. While the EBITDA margin declined by 155 bps YoY and 124 bps QoQ to 23.65% in Q4FY26. PAT for the quarter also declined by -1.87% YoY and +0.16% QoQ.

API segment continued to face pricing headwinds despite volume gains.

While the CDMO segment revenue remain affected in FY26 due to destocking issues and molecule attrition, however, this slowdown was transitional. Further, the demand visibility remained strong despite uncertainties surrounding U.S. tariffs and rising logistics and input costs linked to geopolitical disruptions, as the sector is entering “operational harvesting” phase, where investments made over the past two years begin translating into higher capacity utilization and revenue growth. Moving ahead, strong order visibility and improving execution, the companies are expected to maintain high capital expenditure intensity through FY27.

According the management estimates cement demand for Q4FY26 grew at 6-7% YoY and for full year FY26 grew at 6.5% suggesting a recovery after a subdued H1 which saw a growth of ~5% YoY.

Looking forward, estimates from key cement companies indicated demand growth to be soft (~5%) in FY27 on the back of early forecasts of below normal monsoon which could adversely impact agricultural output and housing demand.

Managements also explicitly called ongoing West Asia conflicts a near term cost shock with increase in cost of key inputs expected to act as a cost moderator.

At aggregate level, the companies saw a 10.39% YoY improvement in revenue with PAT improving 18.84% YoY.

The operating margins came at 17.86%. This represents a decline of 50 bps YoY but an improvement of 263 bps QoQ.

| Company | Y/Y Volume Growth (%) |

|---|---|

| Ultratech Cement | +9% |

| Ambuja Cement | +10% |

| Shree Cement | +9.4% |

| Dalmia Bharat | +3% |

Hospitals sustained healthy double-digit growth in Q4FY26, driven by rising occupancy and improvements in ARPP (Average Revenue per Patient). Capacity-expansion momentum remained strong, with leading chains reaffirming their brownfield and greenfield project pipelines as key growth enablers.

The companies reported a 23.33% YoY increase in revenue, while PAT grew by 21.65% YoY. Operating margin stood at 20.10%, an improvement of 42 bps YoY and 156 bps QoQ.

Apollo Hospitals: Operating beds at the end of quarter was 8,131 beds, a 1.3% YoY increase with occupancy rate of 68% (established units occupancy rate stood at 69%), while the inpatient grew by 7% YoY to 1.57 lakhs. Higher patient intake was further aided by a 9% improvement in average revenue per in patient (ARPP) to Rs.1,87,208 as ALOS fell by 3.3% to 3.19 days.

Max Healthcare: Total beds at the end of Q4 stood at 6,000+ beds, while achieving occupancy levels of 76% FY26. Average Revenue per Operating Bed (ARPOB) for Q4 was Rs 77,900 reflecting a growth of 1% YoY and remained flat on QoQ basis. Inpatient volumes for the quarter were 78,685 (+3.9% YoY but -0.2% QoQ).

Despite the West Asia conflict which triggered higher energy costs, increased freight and logistics expenses, most of the companies managed to clock better margins on account of low cost inventory holding and better product mix.

Domestic demand remained somewhat subdued, impacted by heatwaves affecting agrochemical demand and rural consumption. Meanwhile, the demand from Europe and the US showed a gradual recovery, although it remained uneven and below peak levels, supported by inventory normalization and initial signs of improvement in end-user industries.

Operating margins for the quarter improved to ~17.52%, expanding ~69 bps YoY and ~125 bps QoQ, supported by better realizations and operating leverage.

Revenue for the quarter grew +11.48% YoY, +8.42% QoQ while PAT declined -22.66% YoY and -21.05% QoQ.

Soda Ash: The demand remained stable, with strong domestic demand and subdued international offtake (US glass segment). Recovery is expected to be gradual, supported by solar glass and lithium demand, while prices saw modest increases to offset costs.

Agrochemicals segment: The segment saw mixed performance, with Q4 remaining seasonally weak and impacted by uneven Rabi output. Pricing was firm in select molecules due to supply constraints, while overall demand recovery remained gradual amid weather uncertainties and inventory normalization, keeping the industry in a wait-and-watch phase.

Global crop protection market: The global crop protection market continues to grow at a moderate pace (~5–5.5% CAGR), supported by rising food demand, limited arable land, and increasing focus on productivity enhancement.

Pharmaceutical chemical segment: The pharmaceutical segment continued its robust performance with Advanced Pharmaceutical Intermediates segment growing driven by the CDMO business. Specialty chemicals recorded steady growth while the commodity chemicals subsegment recorded degrowth.

Carbon black: The carbon black segment operated in a volatile environment, impacted by higher feedstock, energy, and logistics costs, which pressured margins. Domestic demand remained stable, supported by the automotive and tyre sectors, while exports were mixed, with weakness in select regions. Ongoing capacity expansion and steady tyre demand helped maintain overall volume stability.

Source: CSEC Research, Bloomberg, NSE, BSE, Corporate Filings • Date: 3rd June, 2026