Industry: Non-Finance Banking Company (Housing Finance Company)

Rating

Accumulate

Investment Horizon

15-16 Months

Date: 16 April, 2026

CMP

Rs. 480.6*

*CMP as of 15th April, 2026 closing

Target

Rs. 600

Potential Returns

+24.8%

Aadhar Housing Finance

Aadhar Housing Finance Limited, incorporated in 1990 and headquartered in Mumbai, is one of India's leading housing finance companies with a strong focus on the low-income housing segment. Initially established as Vysya Bank Housing Finance Limited in Bengaluru, the company underwent several transformations, including its merger with Aadhar Housing Finance Private Limited in 2017, before becoming a public company in May 2024.

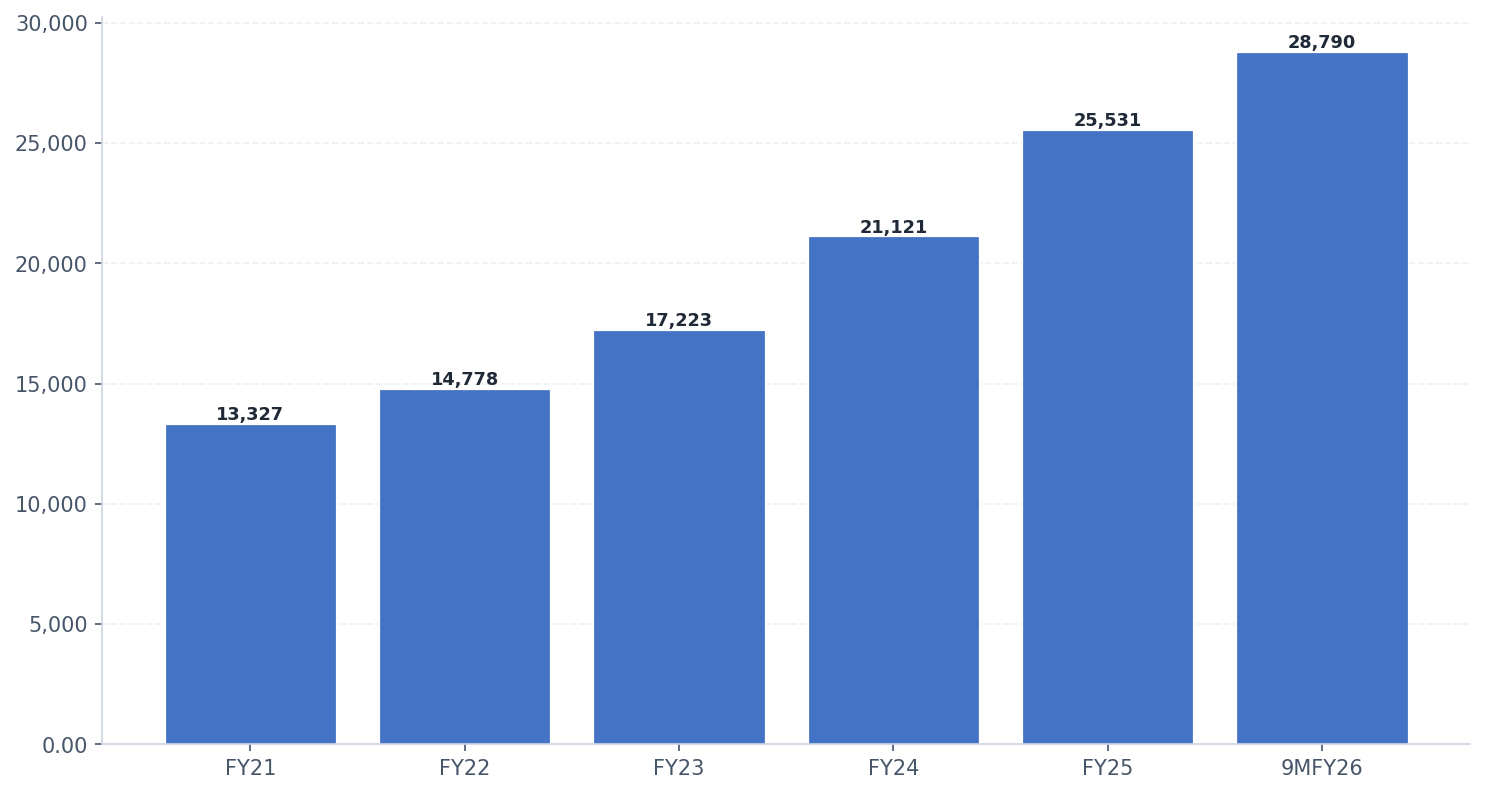

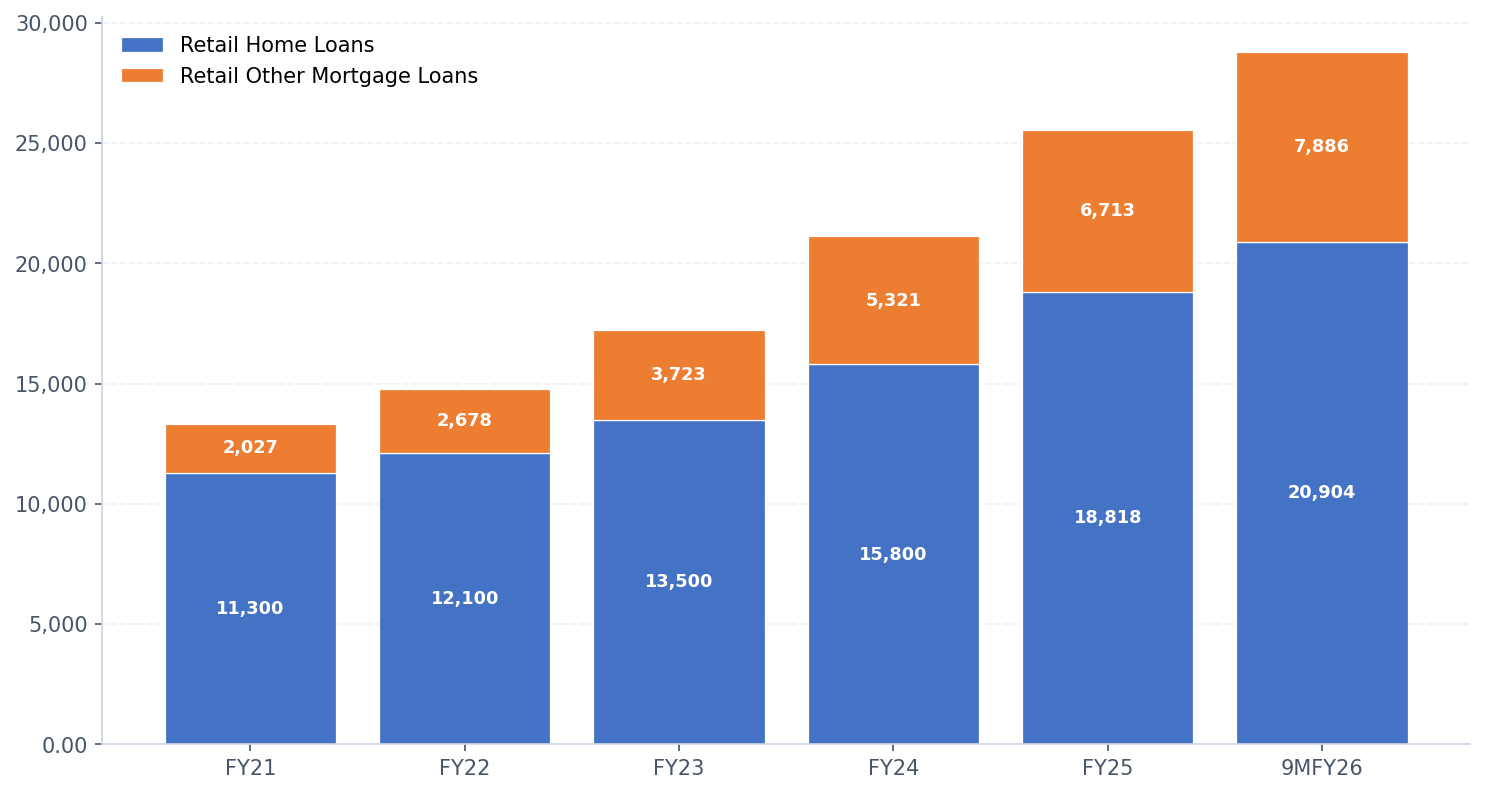

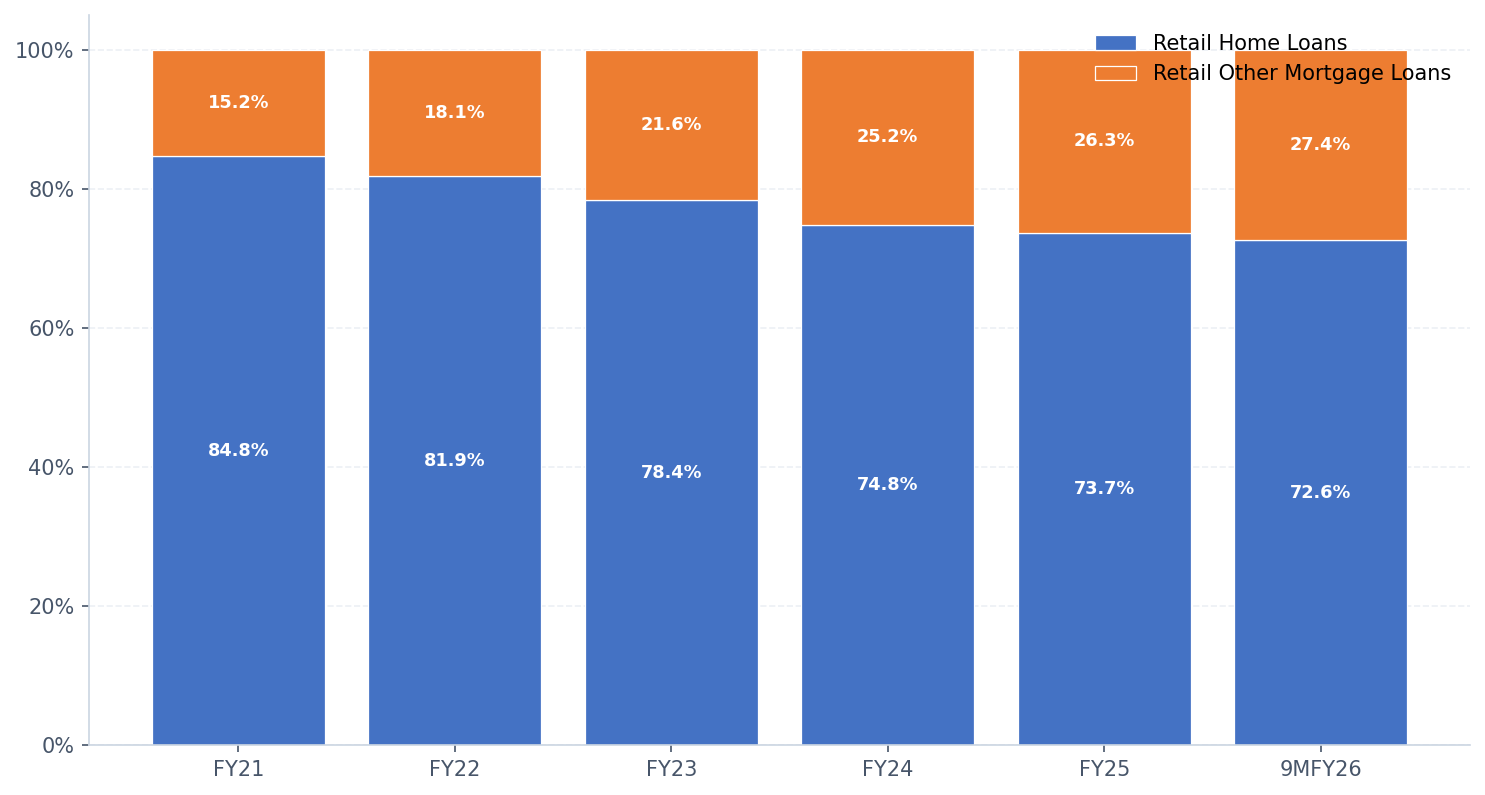

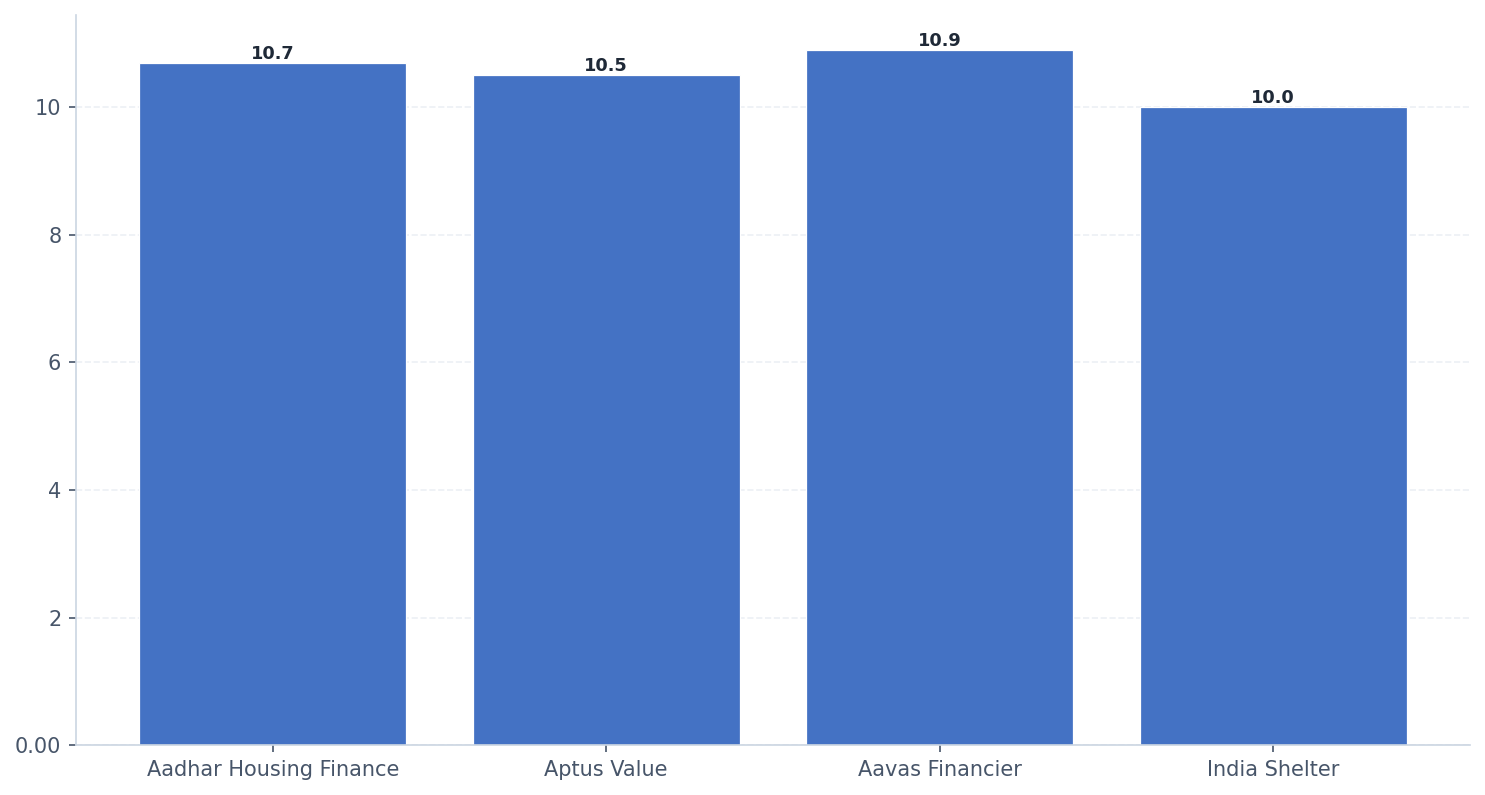

Aadhar specializes in providing small-ticket mortgage loans with an average ticket size of Rs 10.7 lakhs, with almost 64% of its gross AUM directed toward low-income group (LIG) and economically weaker section (EWS) customers. As of 9MFY26, it holds the highest assets under management (AUM) in the affordable housing space at Rs 28,790 crores, with 73% of its portfolio comprising retail home loans and the remaining 23% largely consisting of micro loans against property.

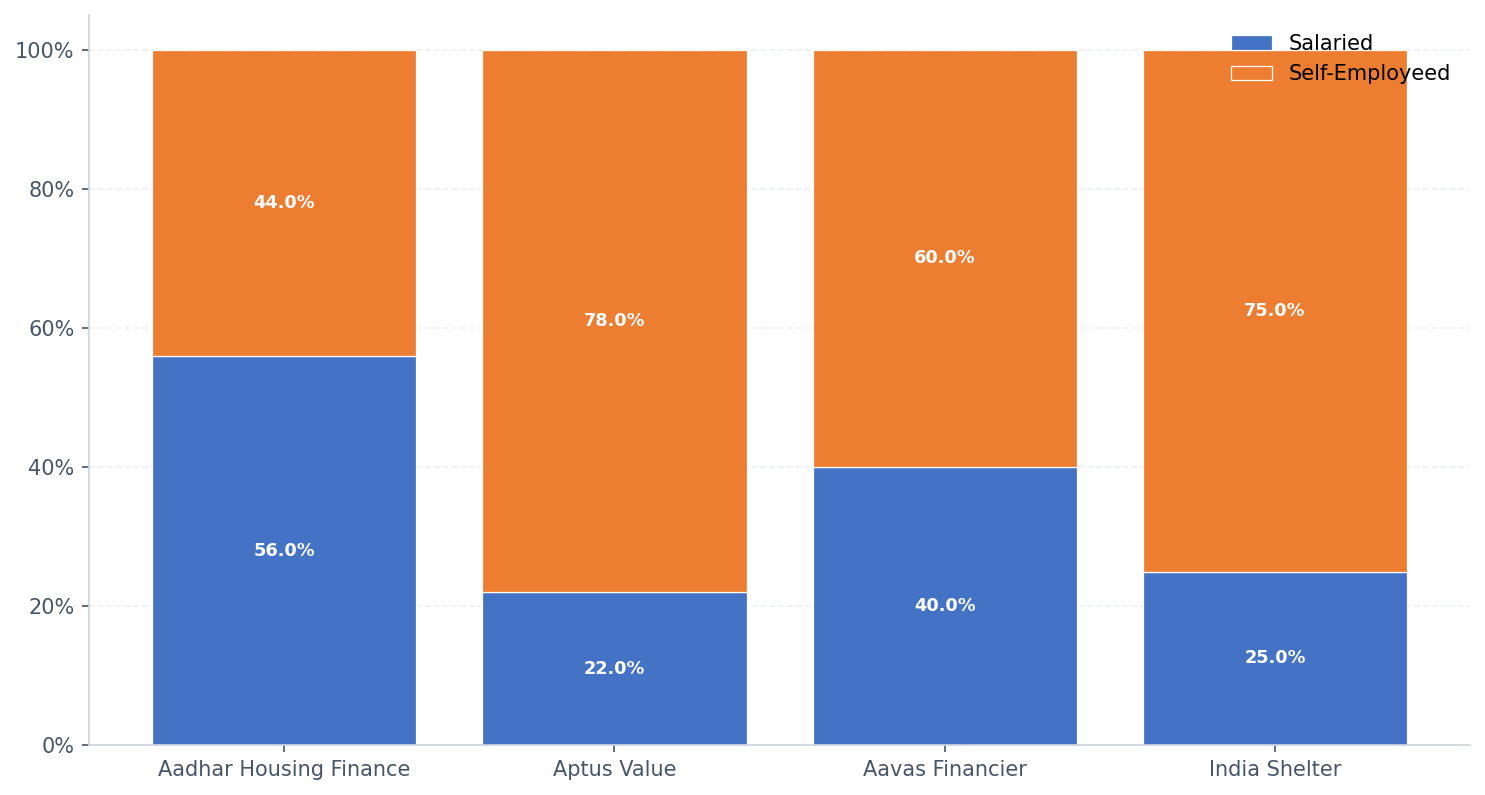

The company operates 620+ branches across 22 states and union territories, serving over 3.24 lakh active accounts, with no single state contributing more than 15% of AUM, ensuring a well-diversified presence. Its origination channels include direct sales teams (43%), the Aadhar Mitra app (22%), and direct selling agents (35%), supported by over 2,600 DST members and 26,000 Mitra connectors. With 55% of its customer base being salaried individuals and 45% self-employed, Aadhar leverages deeper market penetration to offer higher yields compared to peers.

The company maintains a robust long-term credit rating of AA+/Stable from CARE, AA/Positive from ICRA, AA/Positive from India Ratings, underscoring its financial strength and leadership in the affordable housing finance sector.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

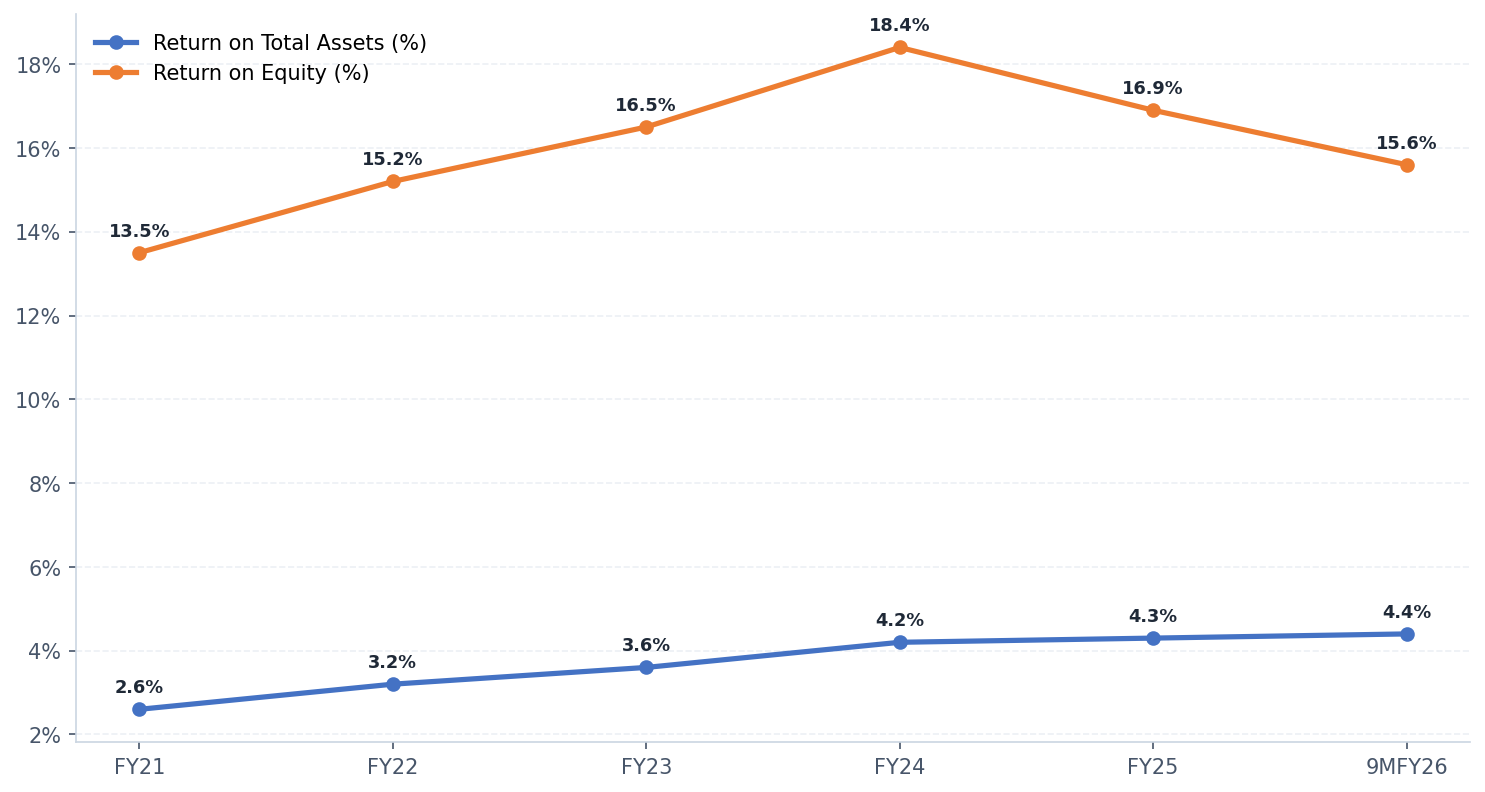

Aadhar Housing Finance presents a compelling investment case, underpinned by its strong growth trajectory, stable asset quality, and prudent risk management practices.

The company reported strong performance in Q3 FY26 and 9M FY26, with assets under management (AUM) rising 20% YoY to Rs 28,790 crore and disbursements growing 15% YoY to Rs 6,469 crore, reaffirming its full-year guidance despite seasonal softness.

The assets under management (AUM) recorded a 20% CAGR over the FY22–FY25 period, rising consistently from Rs 14,778 crores in FY22 to Rs 25,531 crores in FY25.

Its diversified retail secured book, comprising 73% home loans and 27% loan against property (LAP), coupled with an average ticket size of Rs 10.7 lakh and conservative loan-to-value (LTV) ratio of 60%, ensures resilience and sustainability of growth.

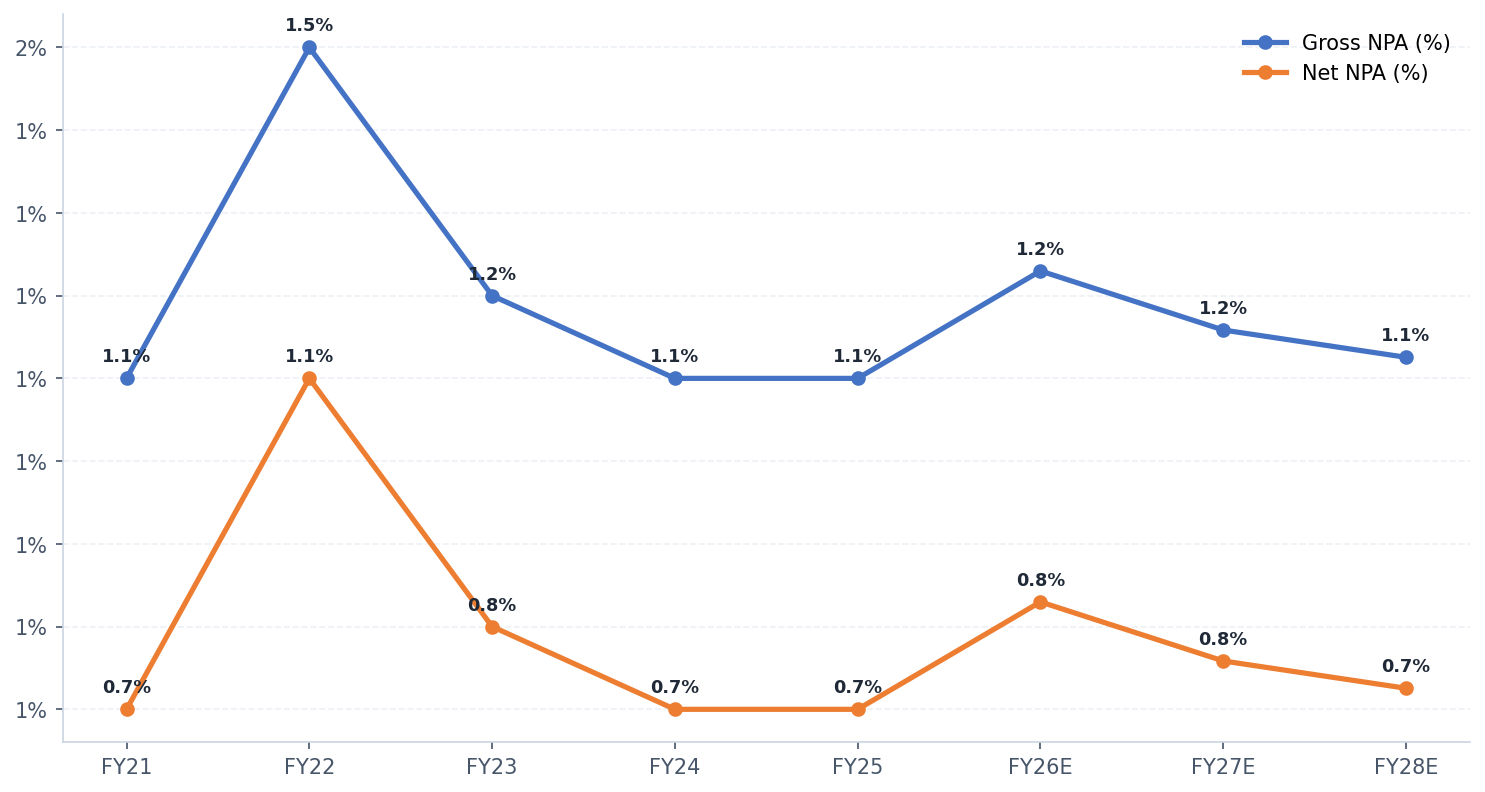

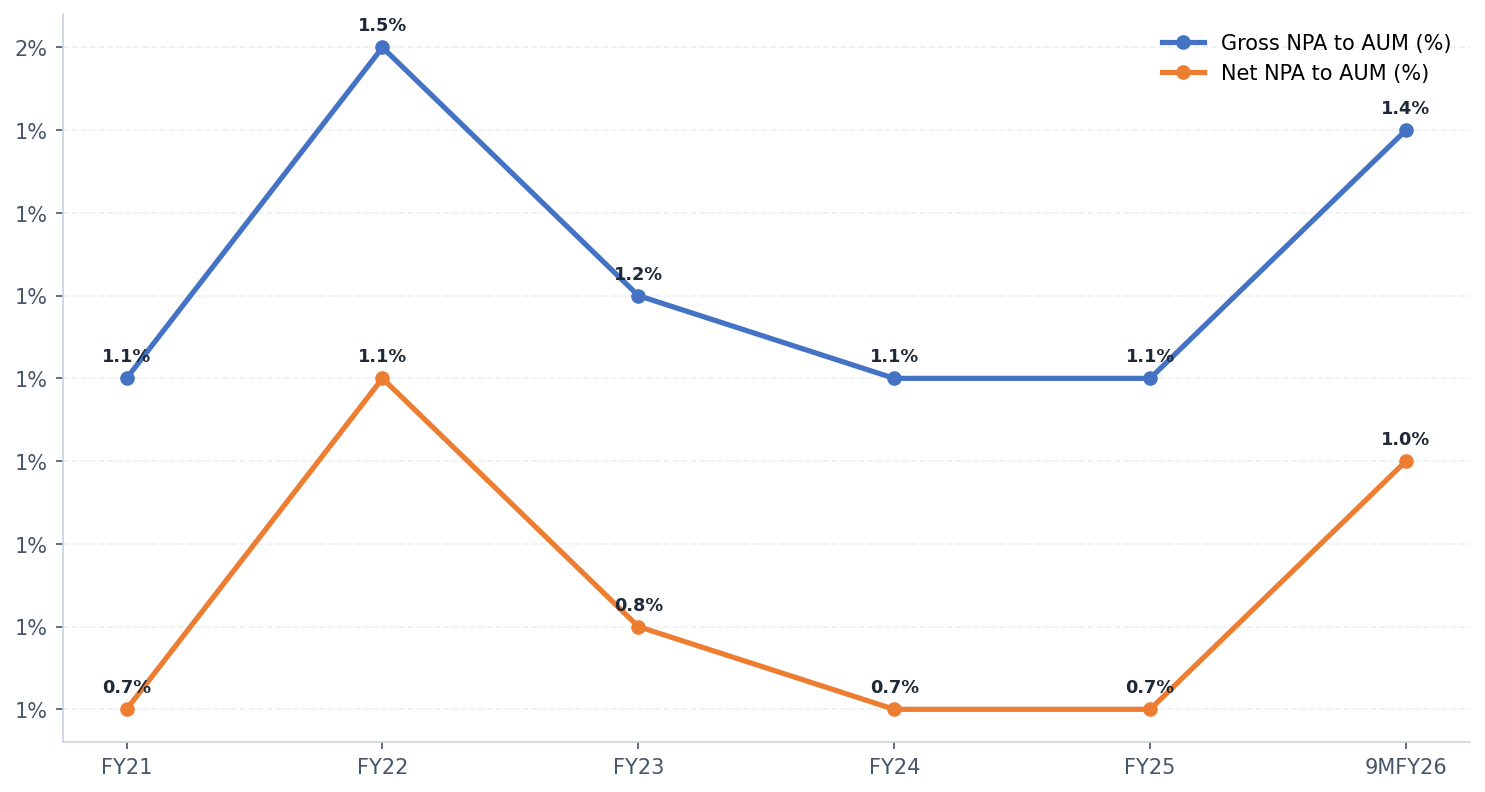

Projected Gross NPA (GNPA) of 1.23% by FY26, indicating prudent underwriting and robust risk management.

Majority of portfolio is salaried customers (55% of AUM), which typically ensures more stable repayment behavior compared to self-employed segments.

Home Loans form a significant portion of the book, with 65% exposure to salaried borrowers, providing resilience and lower credit risk.

Loan Against Property (LAP) contributes 35% salaried exposure, balancing yield and risk.

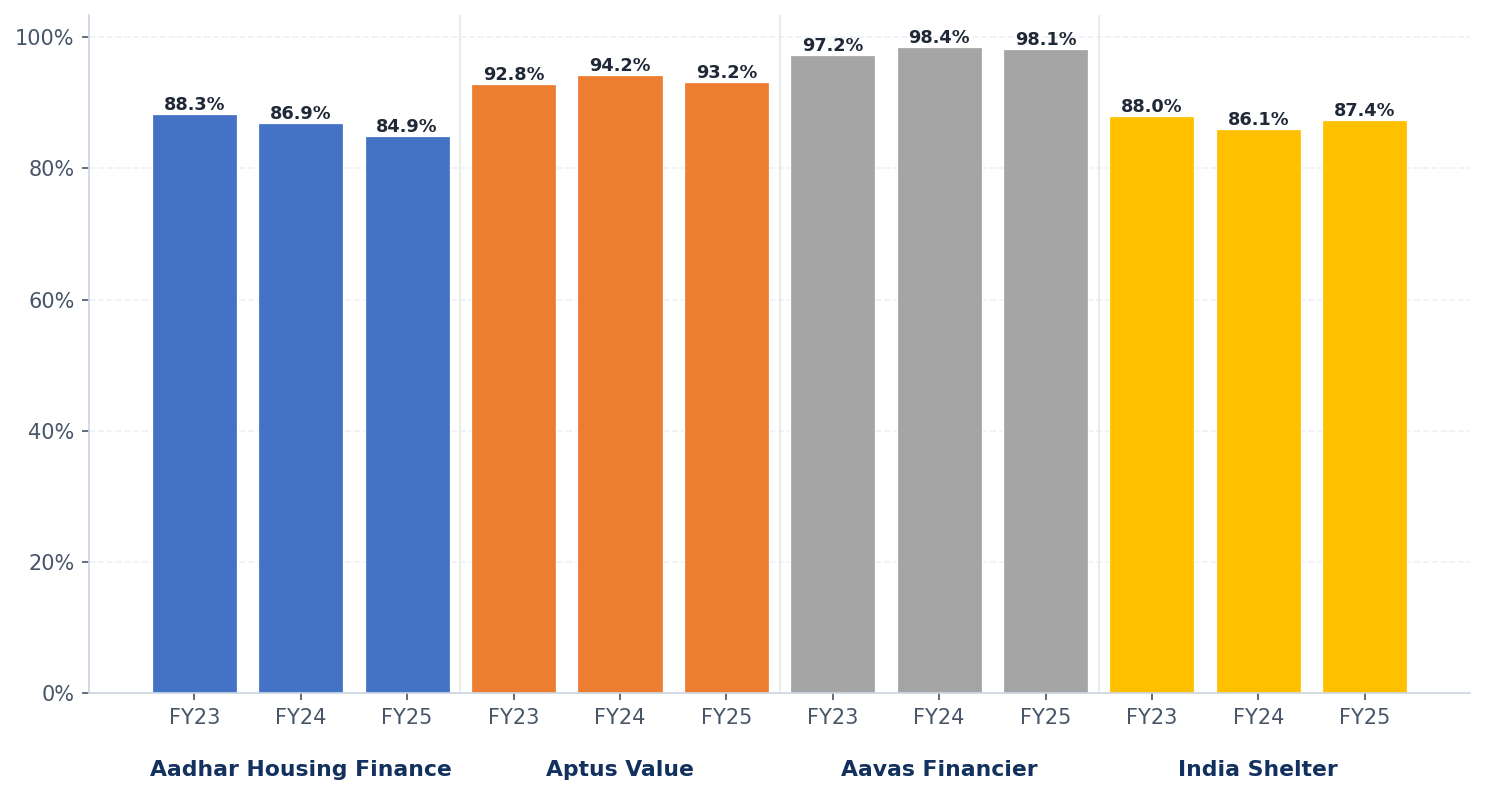

For 9MFY25, Asset quality remains well-managed, with gross NPAs at 1.40% and net NPAs at 1.0%, supported by strong collection efficiency of 98.96% and improving delinquency trends in stressed micro-markets.

(March 2026)

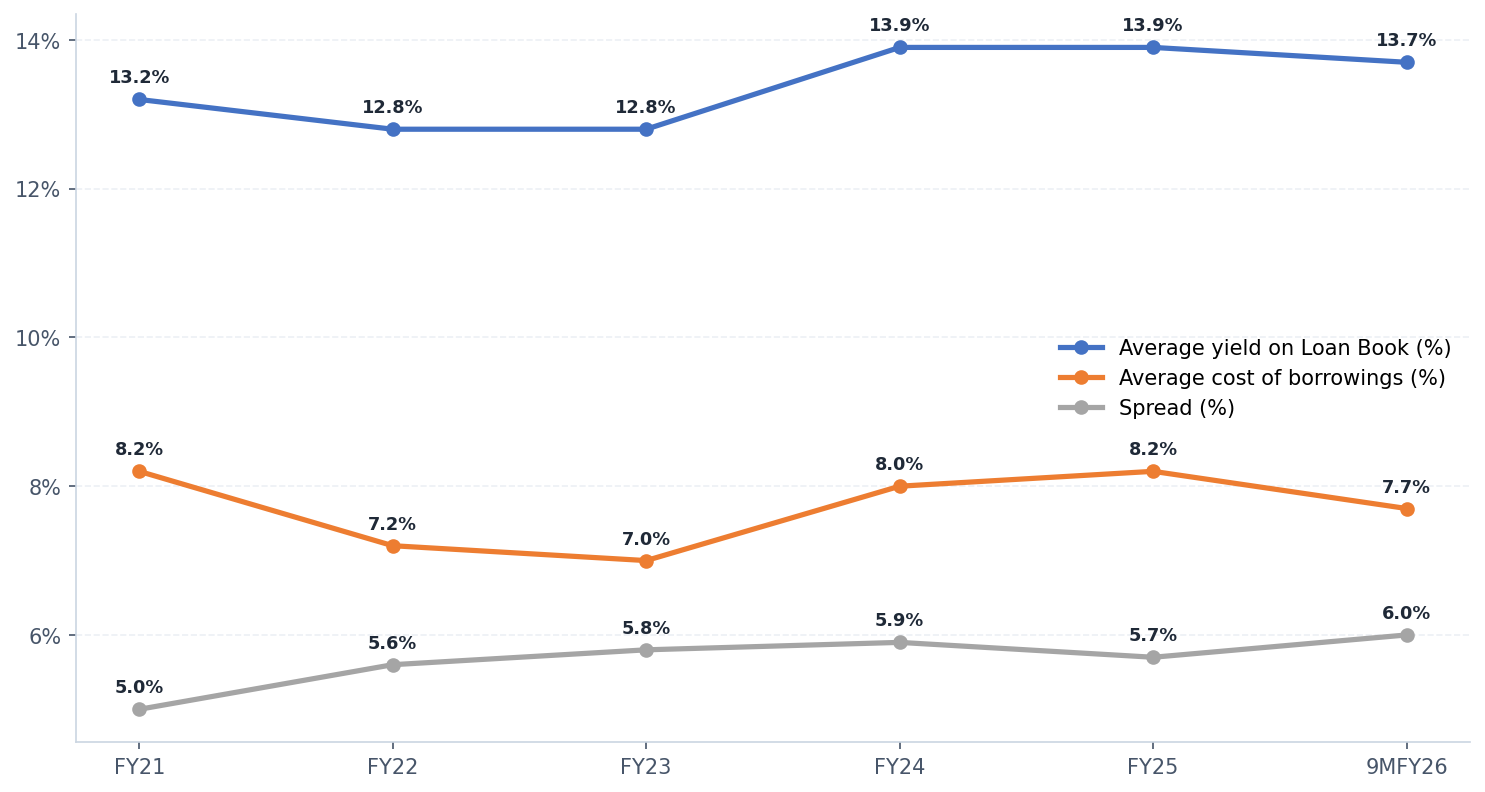

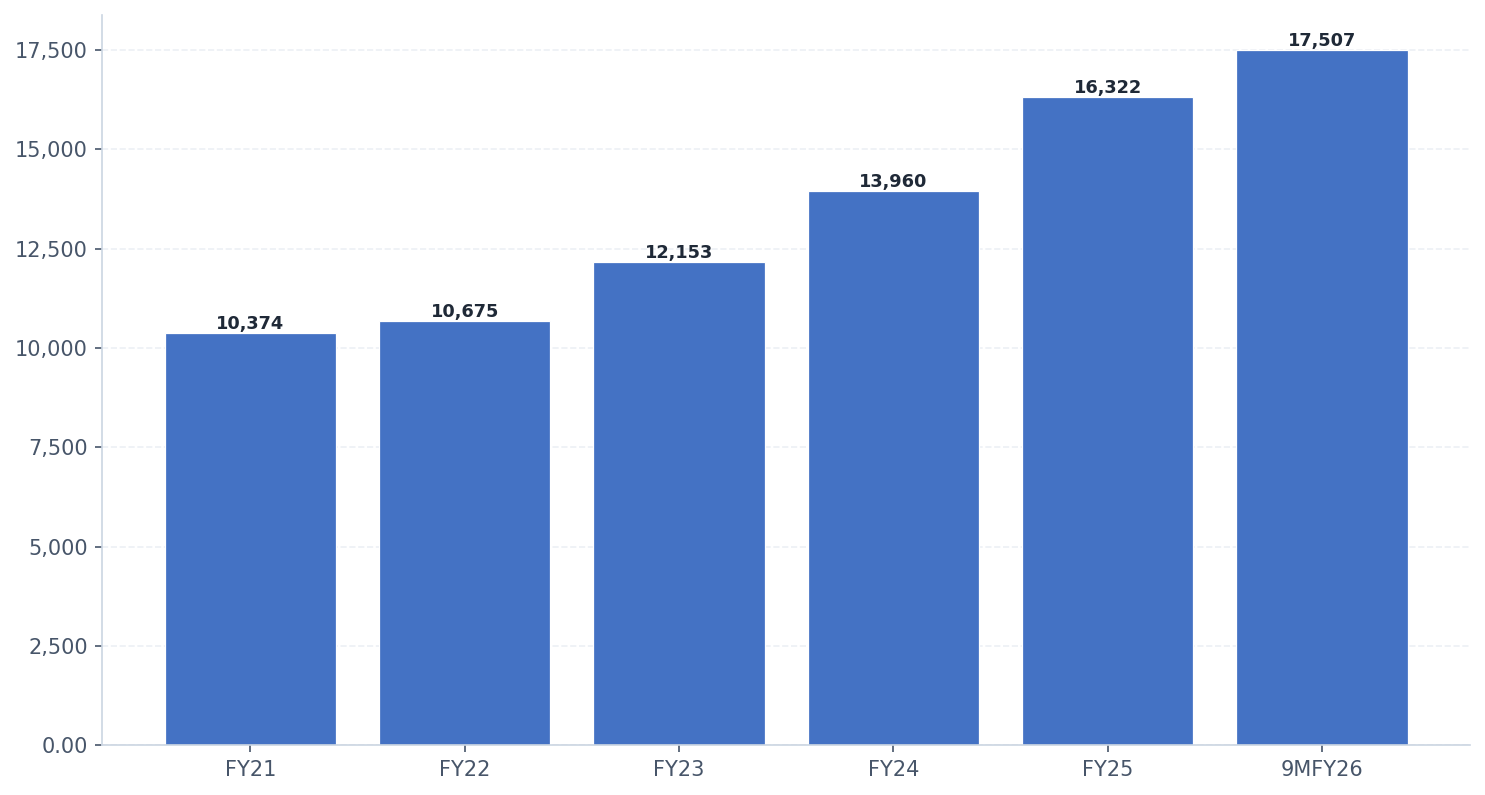

On the funding side, borrowings stood at Rs 17,507 crore (+20% YoY) with a diversified mix, liquidity buffer of Rs 2,400 crore, and cost of funds at 7.7%, expected to improve further.

Strategic initiatives such as expansion under the "urban and emerging" branch strategy, retention efforts for reducing balance transfers, and technology upgrades through TCS-enabled systems and AI/ML adoption further strengthen competitive positioning.

Aggressive branch expansion plan of ~50 new branches every year, supporting consistent growth in customer acquisition and geographical reach. This expansion underpins scalability and strengthens presence in underpenetrated markets.

Additionally, favorable policy tailwinds from GST 2.0 and PMAY 2.0, coupled with management's disciplined stance against rate undercutting, provide a supportive macro environment.

Overall, Aadhar Housing Finance combines scale, geographic diversification, stable asset quality, and strong profitability with clear growth visibility.

With a diversified portfolio where no single state contributes more than 15% of AUM, and a strong foothold in underpenetrated markets, the company has scaled its business faster than peers while mitigating micro-market risks.

As of 9MFY26, it boasts an AUM of Rs 28,790 crores, positioning itself as the leader among listed affordable housing finance companies and commanding a significant share in the low-income housing segment.

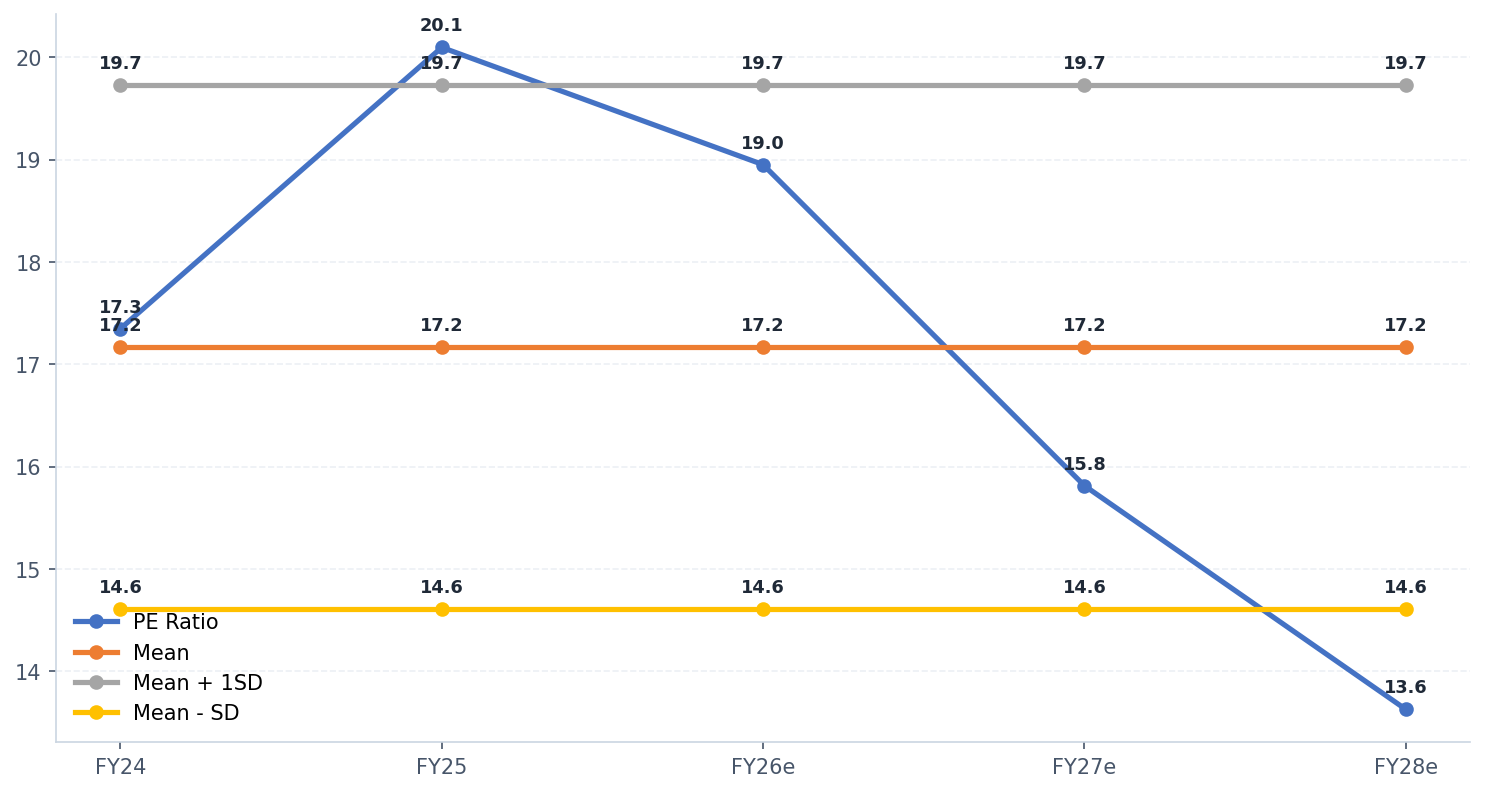

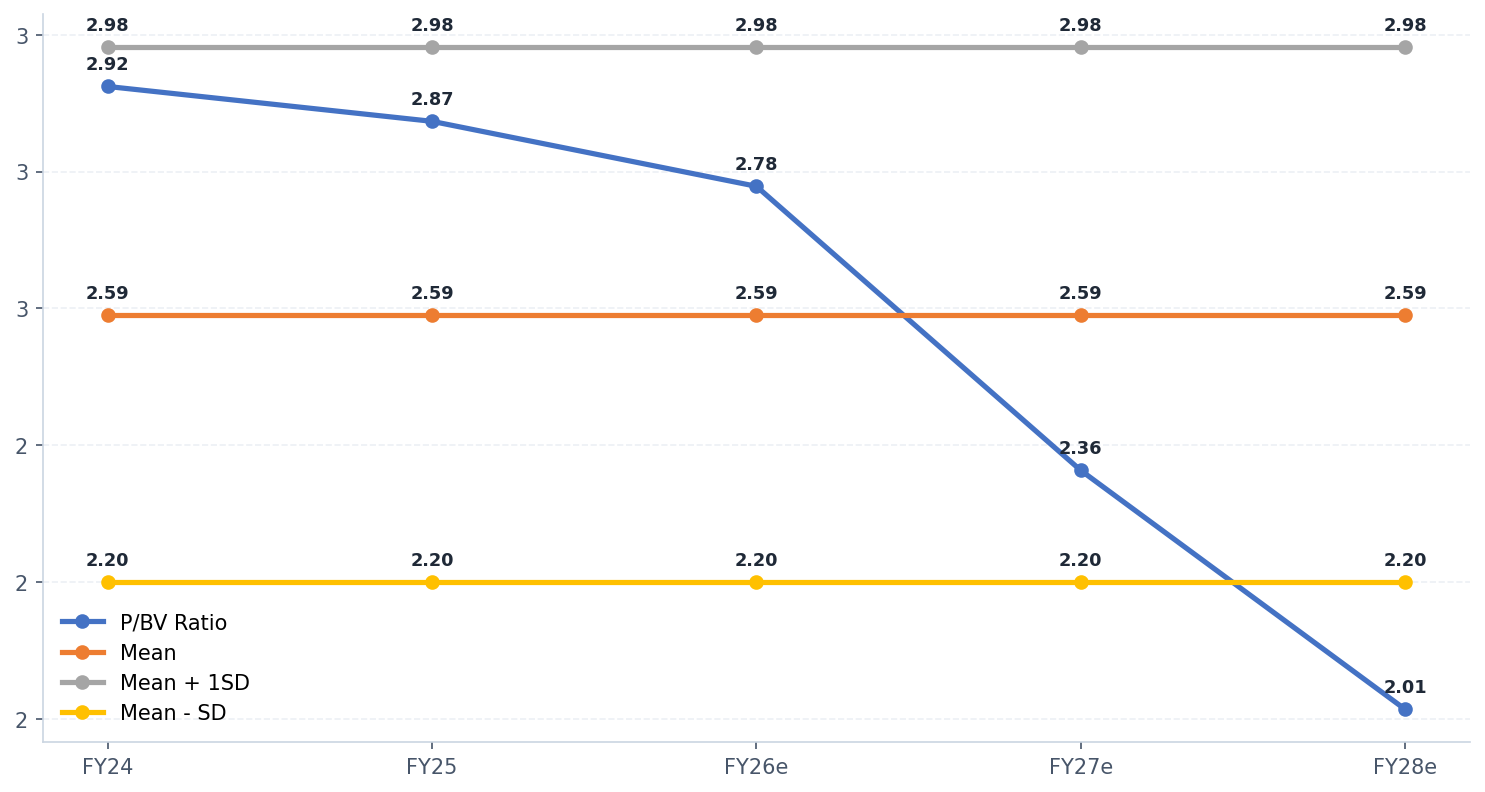

Adopting a conservative approach, valuing the company at a P/BV multiple of 2.5x on FY28e book value, we arrive at a target price of Rs 600 per share, implying a 24.8% upside from the current market price over the next 15–18 months.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

PE & P/BV Ratios are calculated as of 15th April, 2026 closing

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

| Particulars | FY25 | FY26e | FY27e | FY28e |

|---|---|---|---|---|

| Income | ||||

| Revenue from operations | ||||

| a) Interest income | 2,743 | 3,370 | 4,107 | 4,836 |

| b) Fees and commission income | 133 | 174 | 168 | 200 |

| c) Net gain on fair value changes | 22 | 19 | 22 | 27 |

| d) Net gain on derecognition of financial instruments under amortised cost category | 167 | 174 | 179 | 200 |

| Total revenue from operations | 3,065 | 3,737 | 4,476 | 5,263 |

| Other income | 1 | 7 | 4 | 4 |

| Total income | 3,066 | 3,744 | 4,480 | 5,267 |

| Expenses | ||||

| Finance costs | 1,174 | 1,423 | 1,710 | 2,075 |

| Impairment on financial instruments | 57 | 77 | 85 | 101 |

| Employee benefits expense | 407 | 508 | 602 | 695 |

| Depreciation and amortisation | 25 | 32 | 39 | 43 |

| Other expense | 229 | 289 | 345 | 384 |

| Total Expenses | 1,893 | 2,329 | 2,782 | 3,299 |

| Profit before tax | 1,174 | 1,415 | 1,698 | 1,968 |

| Exceptional Item | — | — | — | — |

| Tax expense | 262 | 317 | 382 | 441 |

| Profit after tax | 912 | 1,098 | 1,316 | 1,527 |

| EPS | 21.14 | 25.36 | 30.39 | 35.27 |

| Particulars | FY25 | FY26e | FY27e | FY28e |

|---|---|---|---|---|

| Sources of Funds | ||||

| Share capital | 431 | 433 | 433 | 433 |

| Reserves and surplus | 5,941 | 7,056 | 8,372 | 9,900 |

| Networth | 6,372 | 7,490 | 8,806 | 10,333 |

| Borrowings | 16,322 | 19,595 | 23,818 | 28,951 |

| Trade Payables & Other Liabilities | 514 | 893 | 821 | 535 |

| Derivative Financial Instruments | 15 | — | — | — |

| Total | 23,224 | 27,978 | 33,445 | 39,819 |

| Application of Funds | ||||

| Loan Assets | 20,484 | 24,909 | 29,804 | 35,511 |

| Investments and Cash & Cash Equivalent | 2,237 | 2,491 | 2,980 | 3,551 |

| Other Financial Assets and Trade Receivables | 373 | 425 | 485 | 553 |

| Non-Financial Assets | 131 | 152 | 176 | 204 |

| Derivative Financial Instruments | — | — | — | — |

| Total | 23,224 | 27,978 | 33,445 | 39,819 |

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

| Particulars | FY24 | FY25 | FY26e | FY27e | FY28e |

|---|---|---|---|---|---|

| Earning Per Share (EPS) | 18.99 | 21.14 | 25.36 | 30.39 | 35.27 |

| EPS Growth YoY% | — | 11.32% | 19.96% | 19.84% | 16.04% |

| Price to Earnings (P/E x) | 17.35 | 20.10 | 18.95 | 15.81 | 13.63 |

| Book Value per Share (BVPS) | 112.65 | 147.85 | 172.97 | 203.36 | 238.63 |

| Price to Book Value (P/BV x) | 2.92 | 2.87 | 2.78 | 2.36 | 2.01 |

| Particulars | FY24 | FY25 | FY26e | FY27e | FY28e |

|---|---|---|---|---|---|

| Gross NPA (%) | 1.10% | 1.10% | 1.23% | 1.16% | 1.13% |

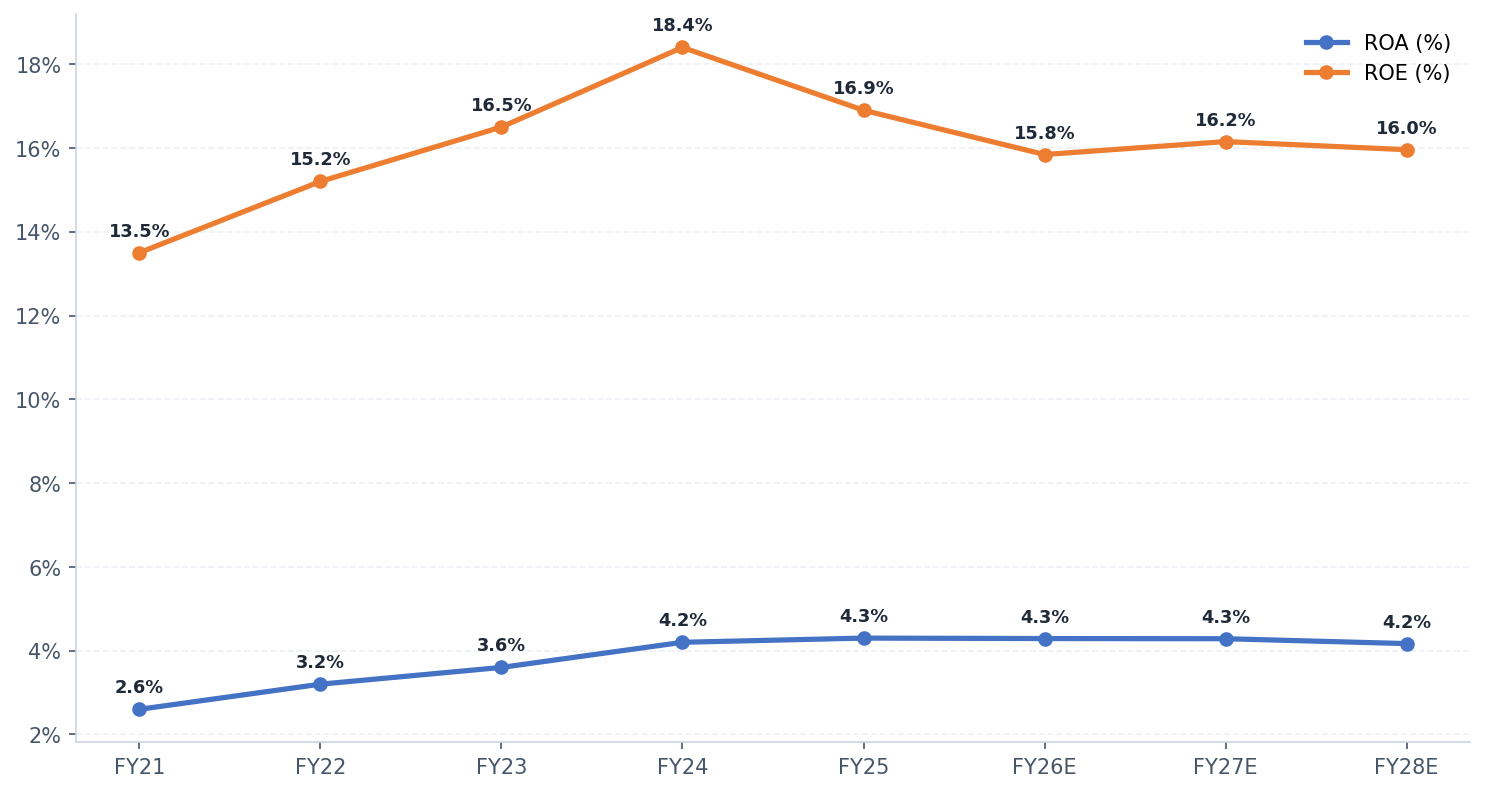

| Net NPA (%) | 0.70% | 0.70% | 0.83% | 0.76% | 0.73% |

| ROA (%) | 4.20% | 4.30% | 4.29% | 4.29% | 4.17% |

| ROE (%) | 18.40% | 16.90% | 15.84% | 16.15% | 15.96% |

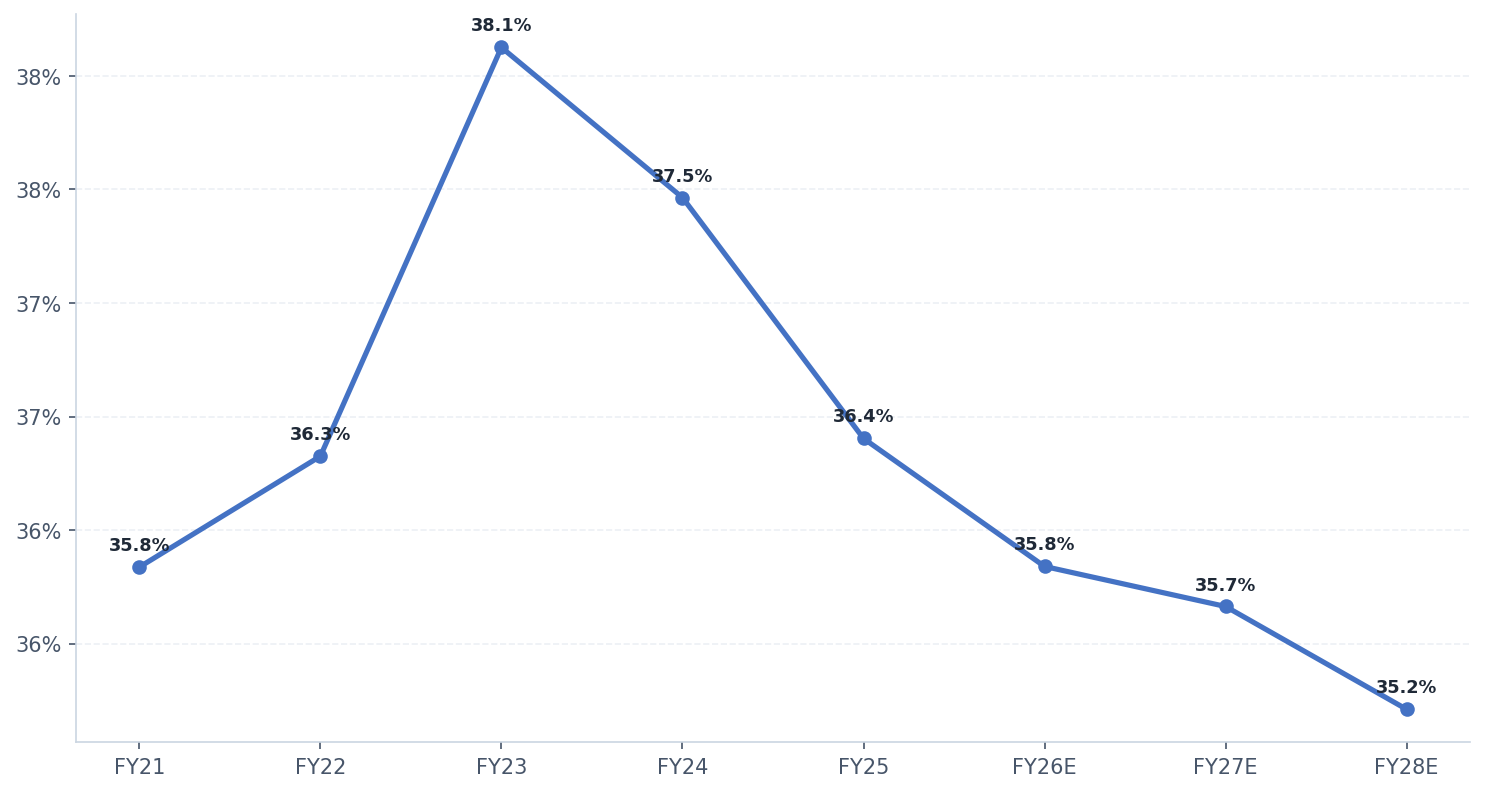

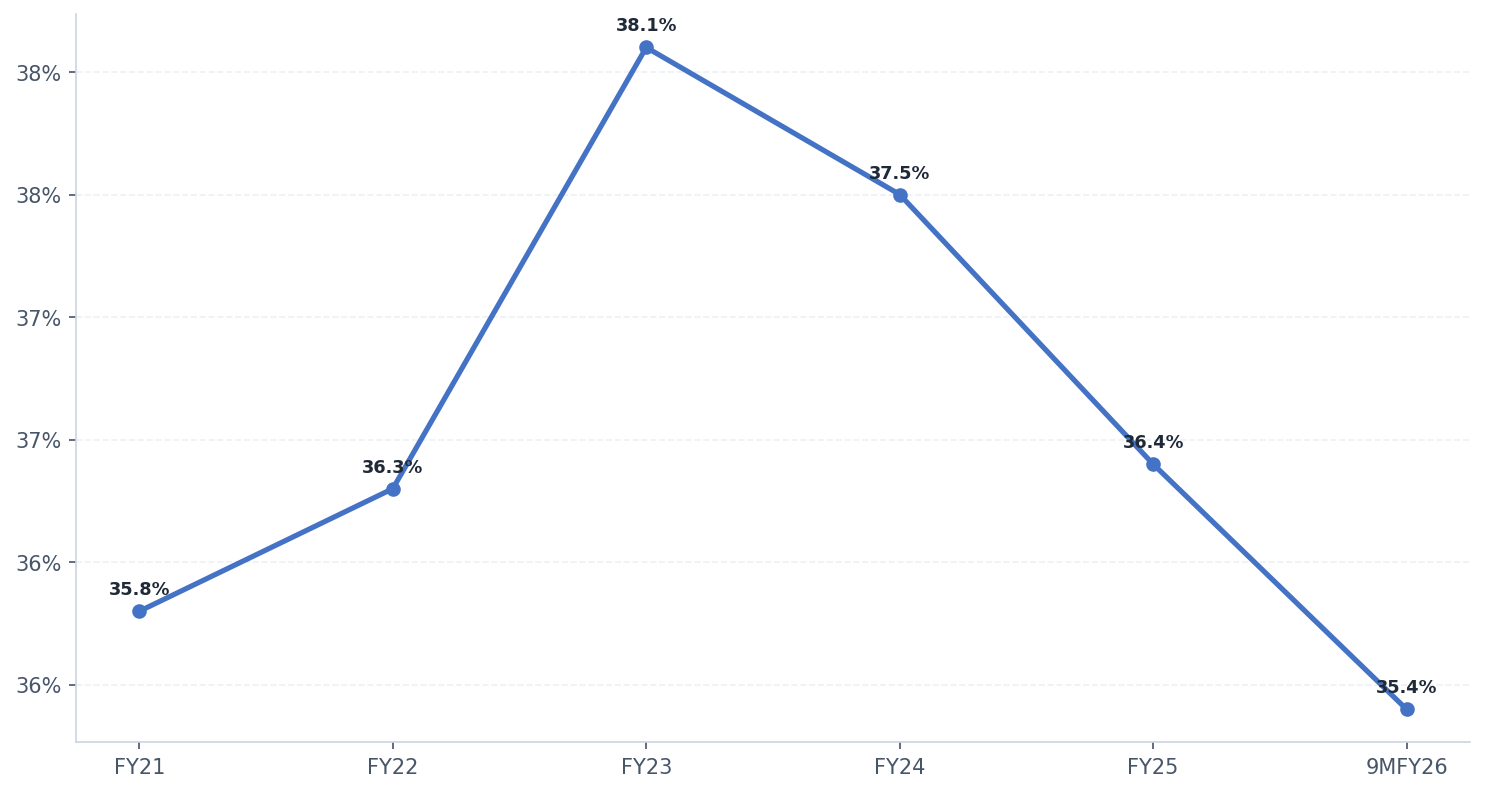

| Cost to Income (%) | 37.46% | 36.40% | 35.84% | 35.66% | 35.21% |

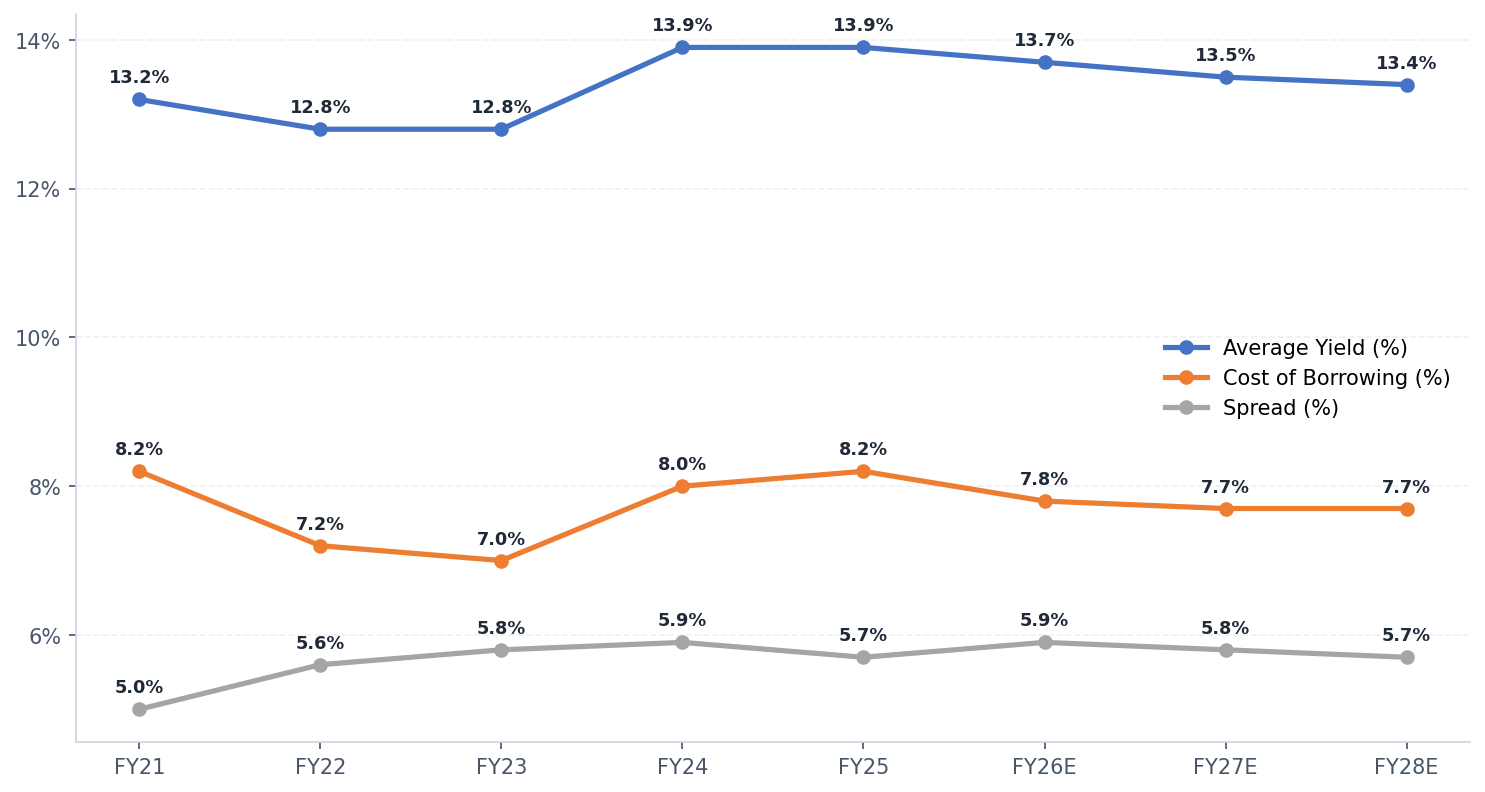

| Average Yield (%) | 13.90% | 13.90% | 13.70% | 13.50% | 13.40% |

| Cost of Borrowing (%) | 8.00% | 8.20% | 7.80% | 7.70% | 7.70% |

| Spread (%) | 5.90% | 5.70% | 5.90% | 5.80% | 5.70% |

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

The segment is designed to cater to the diverse housing needs of low- and middle-income families, with a strong focus on affordability and accessibility. The company offers a wide range of products including Home Purchase Loans for buying residential property, Home Construction Loans for building houses on owned land, and Plot Purchase Loans that allow customers to invest in land for future housing. It also provides a combined Plot Purchase + Construction Loan, simplifying the process by financing both land acquisition and construction under one facility. To support existing homeowners, Aadhar extends Home Improvement Loans for renovation and modernization, as well as Home Extension Loans to help families expand living space with additional rooms or floors. With flexible repayment options, competitive interest rates, and simplified documentation, these products empower economically weaker sections and first-time buyers to achieve housing security while maintaining financial stability.

Aadhar Housing Finance also offers a range of retail other mortgage loan products that provide customers with financial flexibility beyond traditional home loans. Its Loan Against Property (LAP) facility allows borrowers to mortgage their property to access funds for personal or business needs, supporting education, healthcare, or enterprise expansion while retaining ownership of the asset. The company's Balance Transfer option enables customers to shift existing housing loans from other lenders to Aadhar. Additionally, Aadhar provides Commercial Property Construction/Extension Loans, designed for small entrepreneurs and business owners to finance the construction or expansion of shops.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

Nine tailored housing-finance products across the customer journey — from buying land to expanding a business.

Aadhar's Home Purchase Loan helps individuals buy their dream house by offering affordable financing solutions. With flexible repayment options, competitive interest rates, and a focus on low-income and middle-income borrowers, it enables families to own residential property while maintaining financial stability. Documentation is simple, ensuring accessibility for first-time buyers.

This loan supports customers who wish to build their own house on owned land. Aadhar provides funds in stages linked to construction progress, ensuring disciplined usage. With affordable EMIs, transparent processes, and focus on economically weaker sections, it empowers borrowers to create customized homes while maintaining financial comfort and security.

Aadhar offers financing for purchasing residential plots, enabling customers to invest in land for future housing needs. The loan is structured with affordable EMIs, flexible tenure, and transparent eligibility criteria. It helps low- and middle-income families secure land ownership, laying the foundation for building homes at their convenience later.

This combined loan product allows customers to purchase a plot and simultaneously finance construction. It ensures convenience by bundling both requirements into one loan, reducing paperwork and cost. With affordable interest rates and structured disbursements, Aadhar supports families in realizing complete housing solutions, from land acquisition to building their home.

Aadhar's Home Improvement Loan helps borrowers renovate, repair, or upgrade their existing homes. Funds can be used for painting, flooring, plumbing, or modernization. With affordable EMIs and quick processing, it enhances living standards for low-income families, ensuring homes remain safe, functional, and comfortable without straining household budgets significantly.

This loan supports families needing additional space by financing extensions such as extra rooms, floors, or facilities. Aadhar provides affordable repayment options, making it easier for growing households to expand without financial stress. It helps improve living conditions, ensuring families can adapt their homes to evolving lifestyle and space requirements.

Aadhar offers LAP by allowing customers to mortgage their property to access funds for personal or business needs. With prudent loan-to-value ratios and affordable interest rates, it provides liquidity while retaining property ownership. This product supports education, healthcare, or business expansion, ensuring financial flexibility without compromising long-term asset security.

Aadhar's Balance Transfer facility enables customers to shift existing housing loans from other lenders to Aadhar for better terms. Benefits include lower interest rates, reduced EMIs, and improved service quality. This product helps borrowers save money, manage debt efficiently, and enjoy Aadhar's customer-centric approach with simplified transfer processes.

This loan caters to customers seeking funds for constructing or extending commercial properties. Aadhar provides structured financing with affordable EMIs and transparent eligibility, supporting small entrepreneurs and business owners. It enables expansion of shops, offices, or small enterprises, fostering economic growth while ensuring borrowers from weaker sections access formal credit.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

Aadhar Housing Finance has introduced an A–B–C branch categorization system to optimize its reach and efficiency. Category A branches serve as full-service hubs in major urban centers, Category B branches act as mid-level branches in semi-urban areas with moderate operations, and Category C branches are lean, cost-efficient outlets in rural and underserved regions, primarily focused on customer acquisition and servicing. This tiered system allows Aadhar to balance scale, cost, and accessibility while deepening financial inclusion.

The branches are strategically located in metros and large urban centers, functioning as regional hubs with comprehensive operations that include loan origination, credit appraisal, collections, and customer servicing. These branches are staffed with larger teams and equipped with advanced infrastructure to efficiently manage high-value loan portfolios. In addition to their core business functions, Category A branches act as supervisory centers for smaller branches, providing oversight, training, and compliance support. Serving as the backbone of Aadhar's branch network, they play a critical role in ensuring operational excellence and maintaining consistency across the organization's widespread footprint.

The branches are established in tier-2 and tier-3 cities where housing demand is expanding rapidly. These branches provide moderate services, with a primary focus on loan disbursement, customer servicing, and collections. Operating with leaner teams compared to Category A branches, they nonetheless maintain strong customer engagement and play a vital role in building trust at the local level. In addition, Category B branches act as feeder units, channeling complex cases or larger loan requirements to Category A hubs for further processing. By positioning themselves in growing urban clusters and satellite towns, these branches play a critical role in tapping into emerging housing markets and strengthening Aadhar's presence in regions that are driving the next wave of affordable housing demand.

The branches are strategically located in rural, semi-rural, and underserved regions where access to housing finance remains limited. These branches operate with minimal infrastructure and lean staffing, concentrating primarily on customer acquisition, documentation, and servicing. Designed to be highly cost-efficient, they enable the company to expand its footprint without incurring heavy capital expenditure. By focusing on low-income groups (LIG) and economically weaker sections (EWS), Category C branches play a pivotal role in advancing financial inclusion and supporting the government's affordable housing agenda. To enhance efficiency, they often rely on digital tools and centralized processing support from Category A and B branches, ensuring that even remote customers benefit from streamlined services and wider institutional backing.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

Aadhar Housing Finance follows a structured branch expansion strategy, categorising its network into tiers based on annual disbursement volumes. Branches are classified as main branches (annual disbursements above Rs. 24 crore), small branches (Rs. 12–24 crore), micro branches (Rs. 7–12 crore), ultra-micro branches (Rs. 5–7 crore), and deep impact branches, which are sales offices established in remote locations with only 2–3 personnel initially. When entering Tier 4 or Tier 5 markets, Aadhar typically sets up an ultra-micro or deep impact branch staffed by a sales officer and a credit officer. Once the branch achieves a monthly disbursement run-rate of Rs. 0.5 crore (equivalent to 5–7 loan files), it is upgraded to a micro branch, at which point additional staff, including a sales team and an underwriter, are introduced. The target for this upgraded branch is to reach a monthly disbursement run-rate of Rs. 0.8–1 crore within two years, after which it is further upgraded to either a small or a main branch. This tiered approach enables Aadhar to expand efficiently into deeper markets while maintaining the lowest employee-to-branch ratio among its peers.

| Type | Loan disbursal | Typical manpower |

|---|---|---|

| Main Branch | > Rs 24 crores | (a) branch manager; (b)sales team; (c) credit team; (d) technical team; (e) operations team |

| Small Branch | Rs 12 crores to Rs 24 crores | (a) branch manager; (b)sales team; (c) credit team; (d) technical team; (e) operations team |

| Micro Branch | Rs 7 crores to Rs 12 crores | (a) sales manager; (b) DSTs; (c) relationship manager; (d) credit officer |

| Ultra Mirco Branch | Rs 5 crores to Rs 7 crores | (a) sales manager; (b) DSTs or relationship manager |

| Deep Impact Branch | Rs 5 crores to Rs 7 crores | (a) branch in-charge (b) DSTs |

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

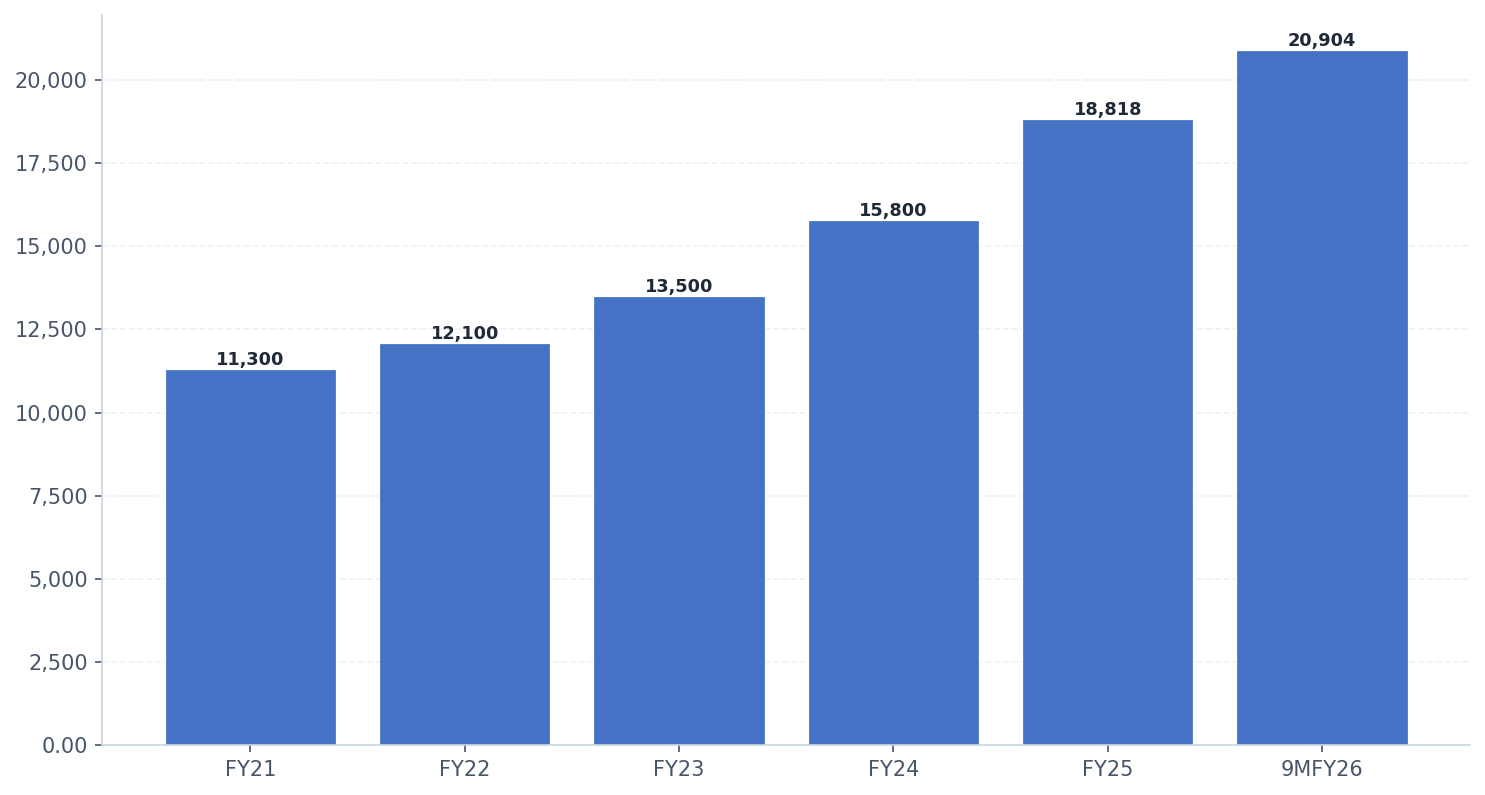

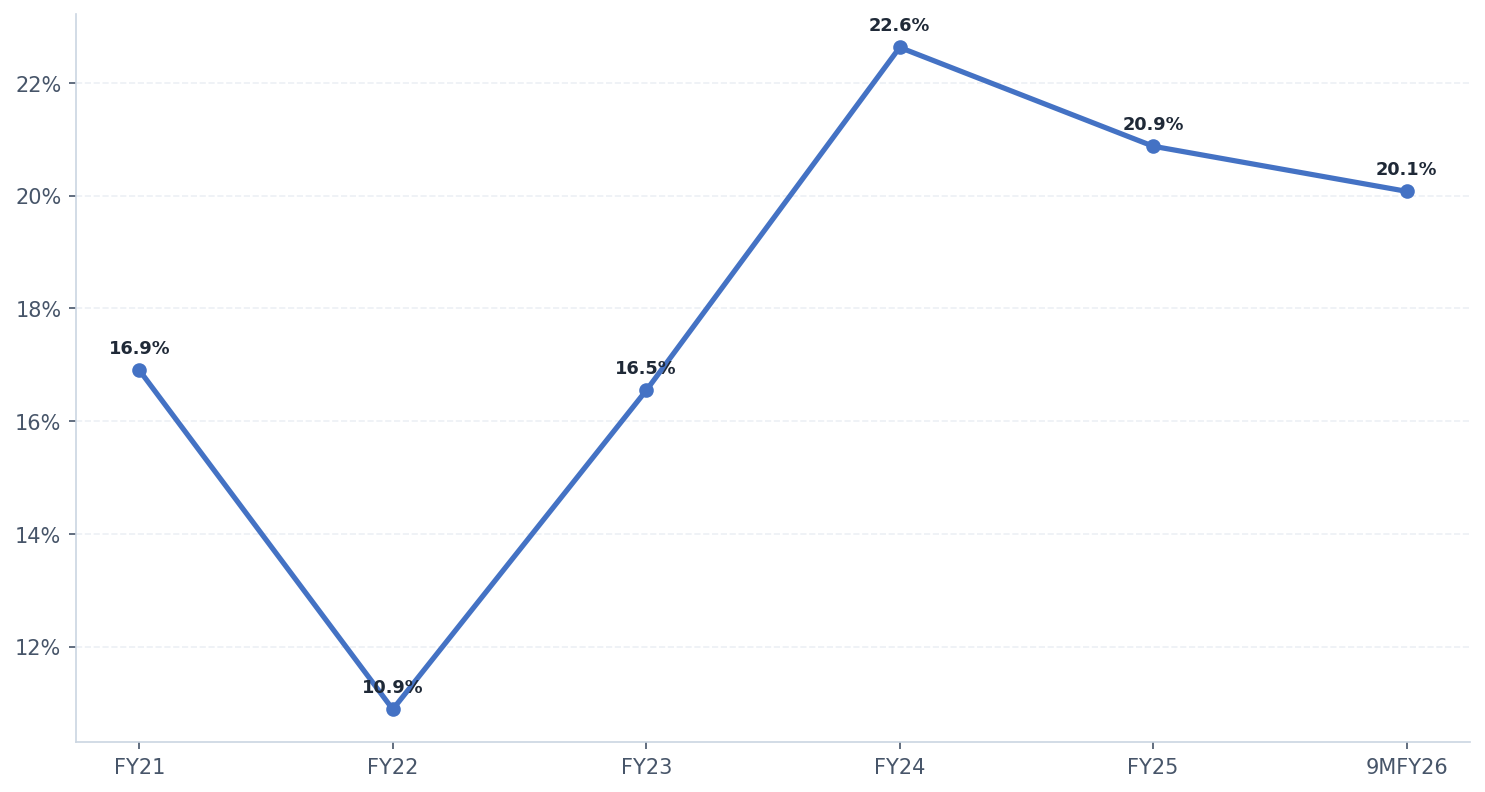

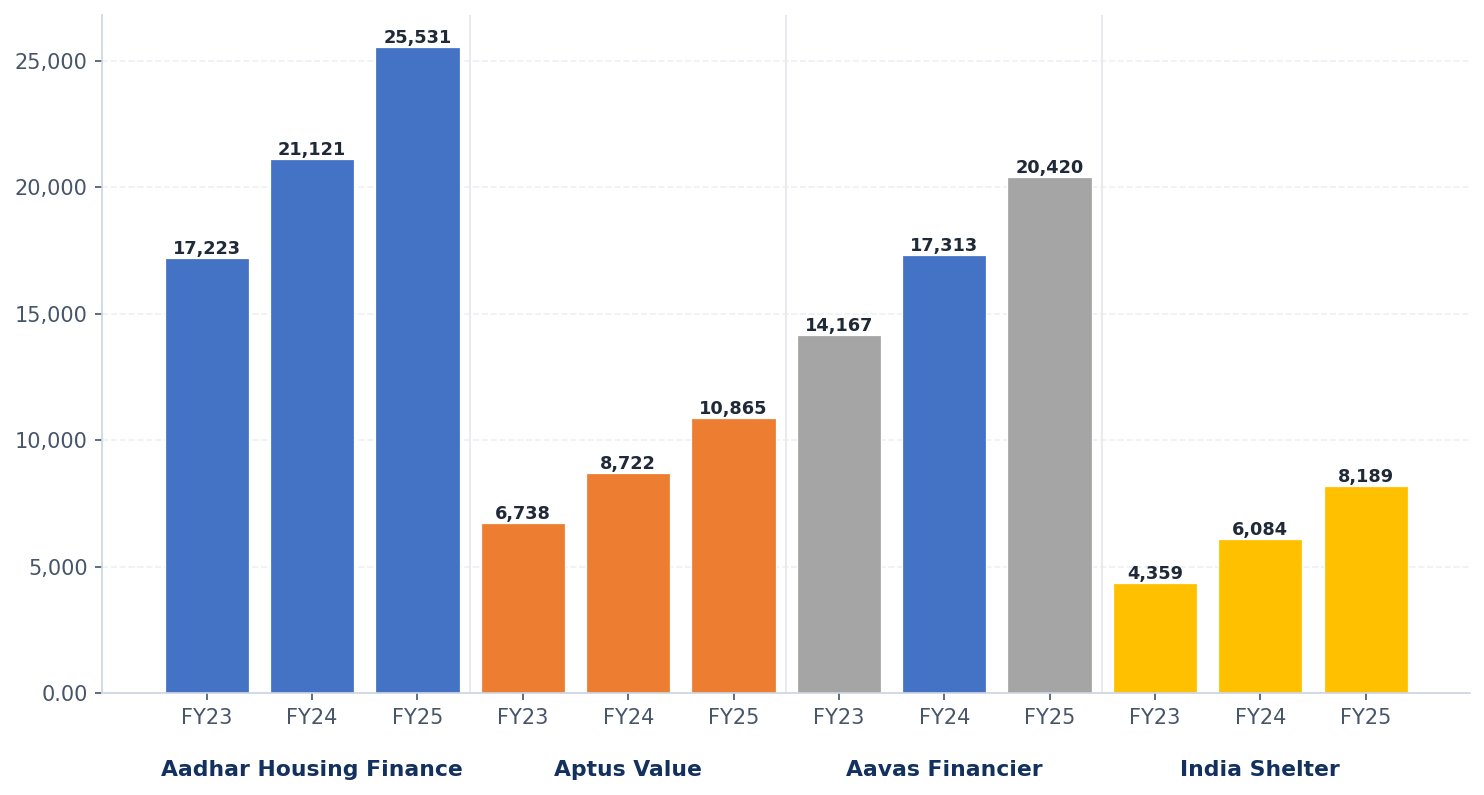

Aadhar Housing Finance has demonstrated consistent and robust growth in its Gross Assets Under Management (AUM) over the past five years, reflecting its expanding footprint in the affordable housing finance segment. The company's AUM has risen steadily from Rs 13,327 crore in FY21 to Rs 25,531 crore in FY25, marking nearly a twofold increase within this period. Growth momentum has been strong, with year-on-year expansion ranging between 10.89% and 22.63%, underscoring both resilience and scalability in its operations.

Notably, FY24 and FY25 recorded significant jumps of 22.63% and 20.88% respectively, highlighting the company's ability to capture rising demand in the housing finance market. As of the 9 months of FY26, Aadhar Housing Finance has already achieved Rs 28,790 crore in AUM, maintaining a healthy growth rate of 20% compared to the previous year. This trajectory indicates sustained business expansion, strong customer acquisition, and effective portfolio management, positioning the company as a leading player in the affordable housing finance sector.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

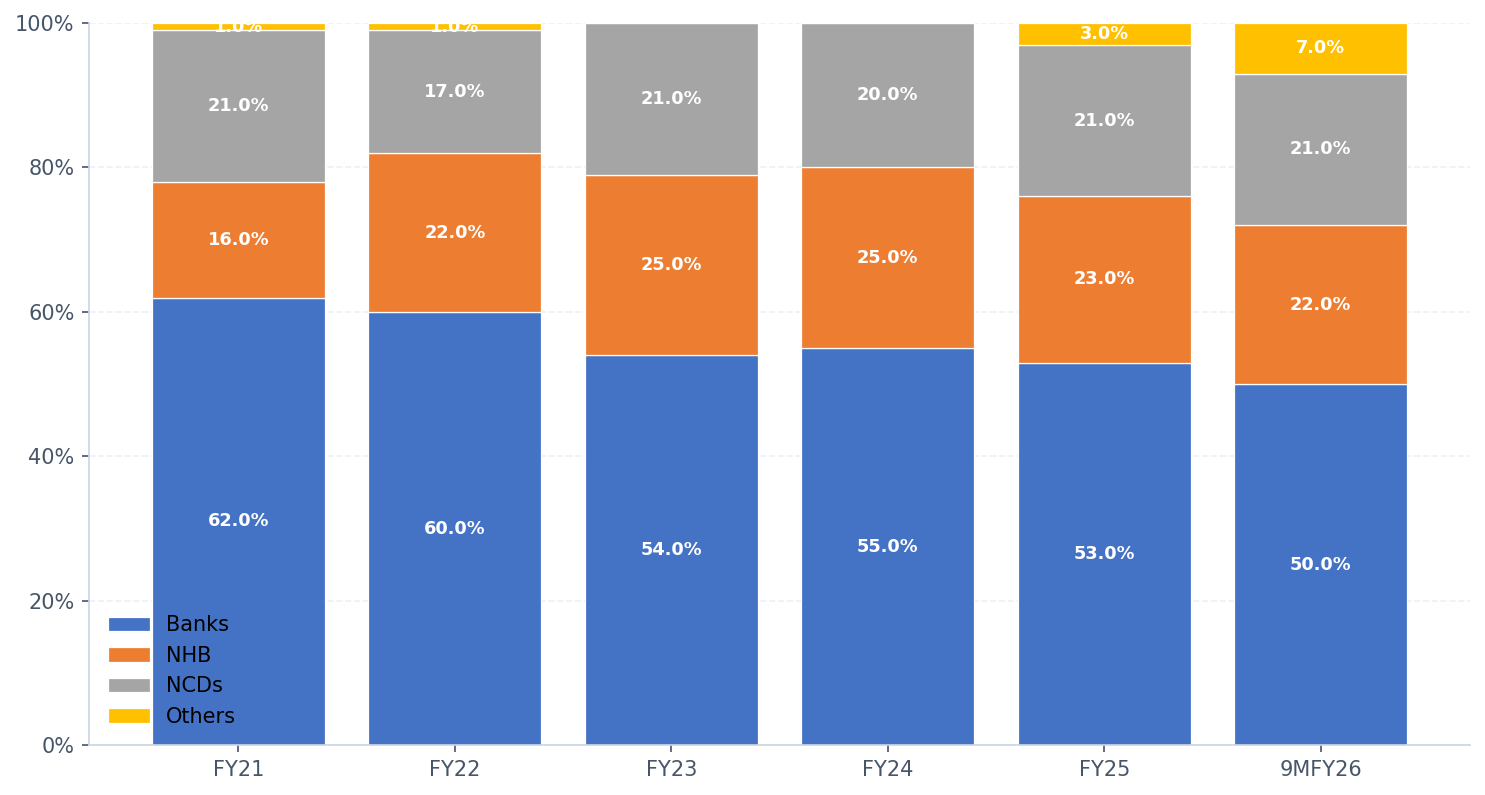

The company also maintains a diversified borrowings mix across 44 lender relationships, with borrowings distributed among banks (50%), NHB (22%), NCDs (21%) and Others (7%). The share of NHB borrowings has risen from 8% in FY20 to 22% in 9MFY26, with half of these borrowings being fixed spread loans directly linked to end-user lending. Overall, 74% of borrowings are floating rate, aligned with 80% of assets being floating rate loans, ensuring smooth transmission of interest rate changes. Aadhar's long-term borrowings carry a robust AA/Stable rating from CARE, Brickwork Ratings, ICRA, and India Ratings, with ambitions to upgrade to AA+ within the next 12–18 months. The company has also entered into a borrowings agreement with the Asian Development Bank (ADB) for USD 60 million, of which USD 30 million was drawn in 1QFY25, and maintains undrawn borrowings of approximately Rs. 900 crores alongside a working capital demand loan facility of Rs. 340 crores.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

The company's growth trajectory is reinforced by favorable government policies and supportive industry dynamics. In the Union Budget 2024–2025, the Pradhan Mantri Awas Yojana–Urban (PMAY-U) received an allocation of Rs. 30,170 crores, marking a 20.19% increase over the previous year.

Under PMAY 2.0, the government has set an ambitious target of constructing 30 million houses by 2029, with interest subsidies of Rs. 1.5 lakh and continued tax incentives for both homebuyers and developers, thereby encouraging housing investments. Industry fundamentals further strengthen Aadhar's positioning, as rapid urbanization, rising disposable incomes, and demographic shifts such as the growing prevalence of nuclear families are driving demand for housing and customized loan products.

The development of satellite cities to ease congestion in major urban centers is expected to further accelerate demand for affordable housing. Despite these strong drivers, India's mortgage-to-GDP ratio remains low at 12.34% as of March 2024, underscoring significant growth potential compared to developed economies.

This under-penetration highlights a substantial opportunity for housing finance companies to expand services, particularly in rural and semi-urban areas where demand is high but access to financing remains limited. Companies like Aadhar are increasingly focusing on underserved populations and low-income segments, thereby advancing financial inclusion and aligning closely with the government's affordable housing agenda.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

Executive Vice Chairman

With a Bachelor's and Master's degree in Science from Lucknow University, Shri Deo Shankar Tripathi has served as the Company's Executive Vice Chairman since 3rd January 2023. He is a Diploma holder in Public Administration from Awadh University and has cleared the associate examination of the Indian Institute of Bankers. He completed various certificate courses, including an International Study Tour on 'Energy Efficiency in Residential Buildings' from KFW Entwicklungsbank, Germany, and a Strategy and Management in Banking Programme from International Development Ireland Limited. Previously, he was a General Manager at Union Bank and President and Chief Operating Officer at DHFL. He also serves as a Director inter alia on the Board of a subsidiary Company, Aadhar Sales and Services Private Limited. He has previously held the position of MD & CEO of the Company.

Managing Director & Chief Executive Officer

With a Post Graduate Certification in Business Management from IIM Kozhikode, Rishi Anand has been serving as the MD & CEO of the Company w.e.f. 3rd January 2023. Prior to his current appointment, he held the position of the COO of Aadhar Housing Finance. He has a rich experience of over 27 years in the financial services sector across a diverse spectrum of functions and businesses. Before joining the Aadhar group, he worked with other companies such as Shelters, ICICI Bank Limited, GE Countrywide Consumer Financial Services Limited, BHW Birla Home Finance Limited, Reliance Capital & AIG Home Finance India Limited, Indo Pacific Housing Finance Limited, and DHFL.

Chief Financial Officer

A qualified Chartered Accountant from the Institute of Chartered Accountants of India and a qualified Cost and Works Accountant from the Institute of Cost and Works Accountants of India, Mr. Rajesh Viswanathan holds a Bachelor's degree in Commerce from the University of Mumbai. He has been an integral part of the Company since 1st December 2019. He has several years of experience in accounting, finance, strategy, planning, taxation, treasury, audit, and managing investor relations. Previously, he has worked at A F Ferguson & Co., Mahindra & Mahindra Limited, DSP Financial Consultants Limited, KPMG Bahrain, Bajaj Allianz Life Insurance Corporation Limited, Bajaj Finance Limited & Capital Float.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

| Particulars | FY23 | FY24 | FY25 |

|---|---|---|---|

| Income | |||

| Revenue from operations | |||

| a) Interest income | 1,776 | 2,275 | 2,719 |

| b) Fees and commission income | 105 | 168 | 199 |

| c) Net gain on fair value changes | 32 | 22 | 22 |

| d) Net gain on derecognition of financial instruments under amortised cost category | 130 | 121 | 167 |

| Total revenue from operations | 2,043 | 2,587 | 3,108 |

| Other income | 0 | 0 | 1 |

| Total income | 2,044 | 2,587 | 3,109 |

| Expenses | |||

| Finance costs | 799 | 987 | 1,174 |

| Impairment on financial instruments | 49 | 41 | 57 |

| Employee benefits expense | 322 | 403 | 407 |

| Depreciation and amortisation | 16 | 21 | 25 |

| Other expense | 136 | 175 | 272 |

| Total Expenses | 1,323 | 1,627 | 1,935 |

| Profit before tax | 721 | 960 | 1,174 |

| Exceptional Item | 25 | — | — |

| Tax expense | |||

| Current tax | 157 | 218 | 249 |

| Deferred tax | -6 | -8 | 13 |

| Profit after tax | 545 | 750 | 912 |

| EPS | 13.80 | 18.99 | 21.14 |

| Particulars | FY23 | FY24 | FY25 |

|---|---|---|---|

| Sources of Funds | |||

| Share capital | 395 | 395 | 431 |

| Reserves and surplus | 3,303 | 4,055 | 5,941 |

| Networth | 3,698 | 4,450 | 6,372 |

| Borrowings | 12,153 | 13,960 | 16,322 |

| Trade Payables & Other Liabilities | 766 | 683 | 514 |

| Derivative Financial Instruments | — | — | 15 |

| Total | 16,618 | 19,093 | 23,224 |

| Application of Funds | |||

| Loan Assets | 13,851 | 16,903 | 20,484 |

| Investments and Cash & Cash Equivalent | 2,377 | 1,735 | 2,237 |

| Other Financial Assets and Trade Receivables | 267 | 285 | 373 |

| Non-Financial Assets | 122 | 170 | 131 |

| Derivative Financial Instruments | — | — | — |

| Total | 16,618 | 19,093 | 23,224 |

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

India faces a significant housing shortage, particularly in states with lower per capita income and higher population density. As per the Twelfth Five Year Plan (2012–2017), ten states accounted for nearly 76% of the total urban housing shortage. Uttar Pradesh alone has a shortage of over 3 million homes, followed by Maharashtra (1.94 million), West Bengal (1.33 million), Andhra Pradesh (1.27 million), and Tamil Nadu (1.25 million). Several of these states, including Uttar Pradesh, Bihar, West Bengal, Rajasthan, and Madhya Pradesh, have per capita incomes below the national average, underscoring the dual challenge of affordability and access.

India's housing finance ecosystem is characterized by the dual presence of banks and housing finance companies (HFCs), with banks holding nearly three-fourths of the overall housing loan portfolio as of FY2024. HFCs, however, play a critical role in catering to niche borrower segments, particularly in semi-urban and rural markets, and among self-employed individuals with informal income documentation. Their ability to design flexible loan products and deliver last-mile credit has positioned them as key enablers of affordable housing finance, complementing the reach of banks.

The majority of the housing shortage lies in the low-income group (LIG) and economically weaker section (EWS) segments, with only 5–7% in the middle-income group (MIG) or above. Addressing this shortage would generate incremental housing loan demand estimated at Rs. 50–60 lakh crores, compared to the overall housing loans outstanding of Rs. 31.1 lakh crores (excluding PMAY loans) as of March 2023. The RBI-appointed Committee on Housing Finance Securitisation (Sep 2019) further estimated that fulfilling the entire shortage would require units valued at Rs. 149 lakh crore, with aggregate loan demand of Rs. 58 lakh crore, highlighting the immense latent potential of the market.

HFCs have historically grown at a slower pace compared to banks, with housing loan portfolios expanding at ~12% CAGR between FY2019 and FY2025, versus ~17% CAGR for banks. Despite this, HFCs remain strategically important in addressing the housing shortage concentrated in the economically weaker section (EWS) and low-income group (LIG) categories. Government schemes such as the Credit Linked Subsidy Scheme (CLSS) under PMAY, Affordable Housing in Partnership, and refinance support from the National Housing Bank (NHB) have further strengthened the role of HFCs in delivering affordable housing finance.

The sector's growth drivers include rapid urbanization, rising demand from Tier-II and Tier-III cities, and increasing adoption of digital underwriting and alternative credit assessment tools. HFCs are also leveraging partnerships with microfinance institutions (MFIs), fintechs, and NBFCs to expand their reach into underserved geographies.

India's mortgage market is broadly divided by ticket size, with loans above Rs. 1.5 crore dominating metro and urban markets, while loans of Rs. 1.5 crore and below cater to semi-urban and rural areas and form the backbone of the low-income housing segment. This latter segment is the primary focus of government schemes such as Affordable Housing in Partnership, the Credit Linked Subsidy Scheme (CLSS) under PMAY, and refinance support from the National Housing Bank's Affordable Housing Fund.

According to the RBI Committee report (2019), the housing shortage is concentrated in the EWS and LIG categories, with 4.5 crore houses needed in the EWS segment and 5 crore in the LIG segment. Recent industry trends further highlight value growth despite volume slowdown, with rising ticket sizes and luxury housing demand driving overall market expansion.

In conclusion, while banks will continue to dominate the housing finance market, HFCs will play an indispensable role in driving financial inclusion and supporting India's vision of "Housing for All." By addressing affordability challenges, innovating credit delivery, and aligning with government initiatives, HFCs will remain catalysts of social and economic transformation, contributing significantly to GDP growth, urban development, and improved living standards across the country.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

The company along with its subsidiary Aptus Finance India Private Limited, is a leading provider of housing finance solutions in India. Incorporated in 2009 and headquartered in Chennai, the company focuses on serving low and middle‑income families, self‑employed individuals, and first‑time homeowners in rural and semi‑urban areas. Its offerings include home and quasi‑home loans for purchase, construction, renovation, and extension of houses, loans against property, and secured small business loans.

The company incorporated in 2011 and headquartered in Jaipur, is a leading housing finance company catering to low- and middle-income customers in semi-urban and rural India. The company provides diverse loan products including home loans for flats, houses, bungalows, and resale properties; construction loans for self-built homes; and home improvement loans for repairs and renovations. It also offers loans against property, MSME loans, balance transfers, and small-ticket financing solutions.

The company was incorporated in 1998 and headquartered in Gurugram, is a housing finance company dedicated to enabling affordable home ownership across India. The company provides a range of financial products including home loans for purchase and construction, renovation loans, and loans against property. Serving primarily low- and middle-income customers, India Shelter focuses on semi-urban and rural markets where access to formal credit is limited.

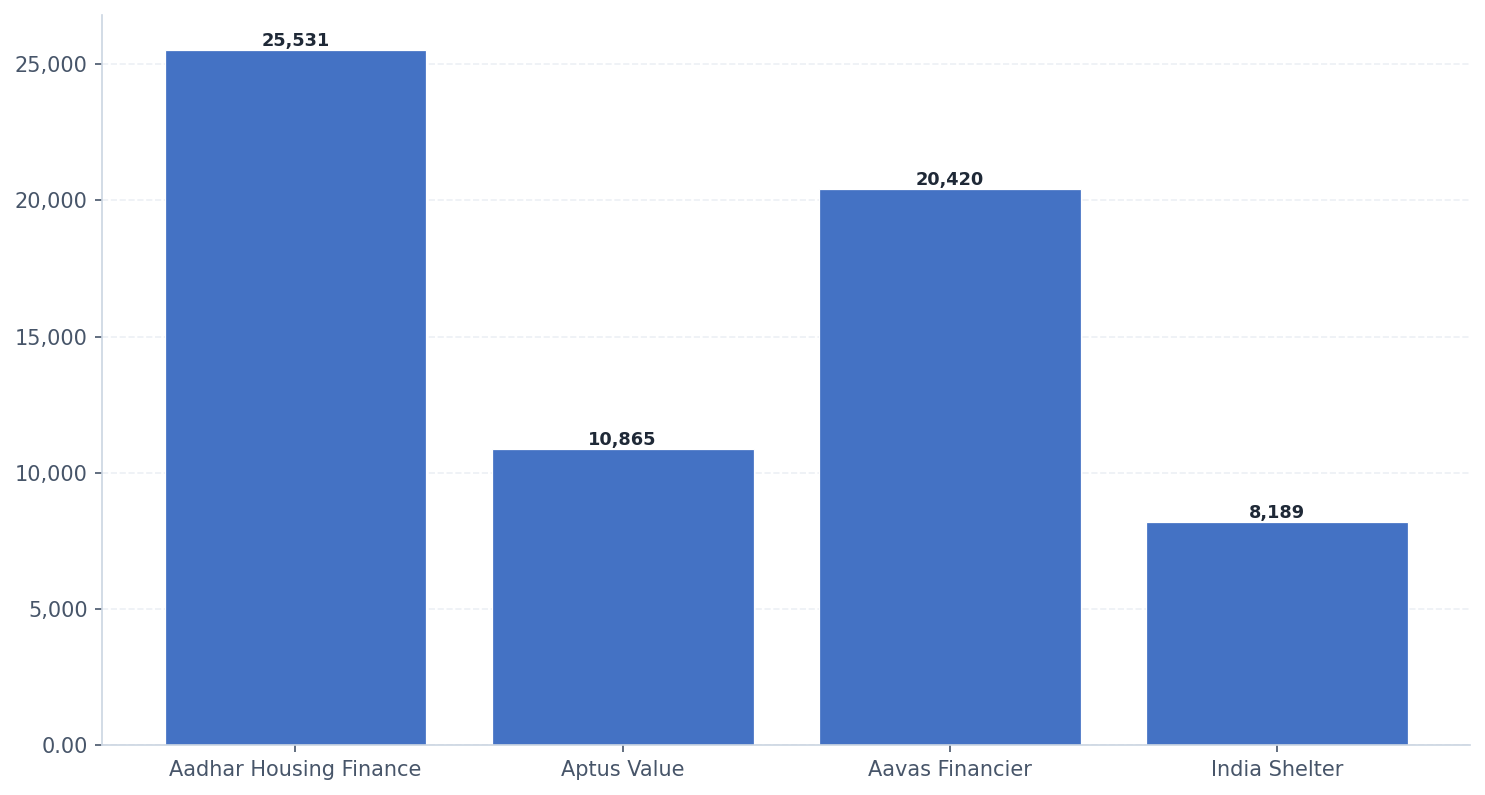

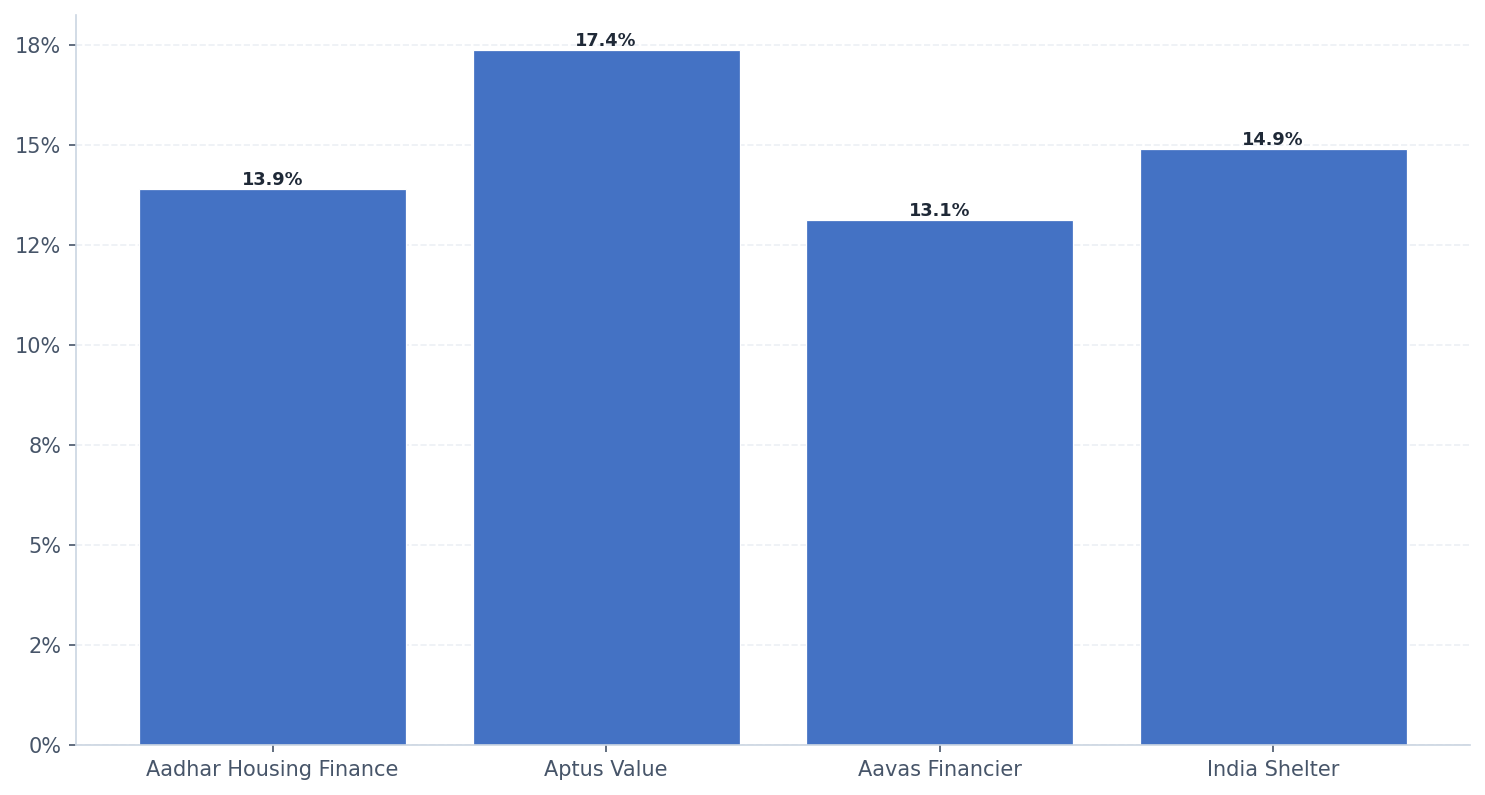

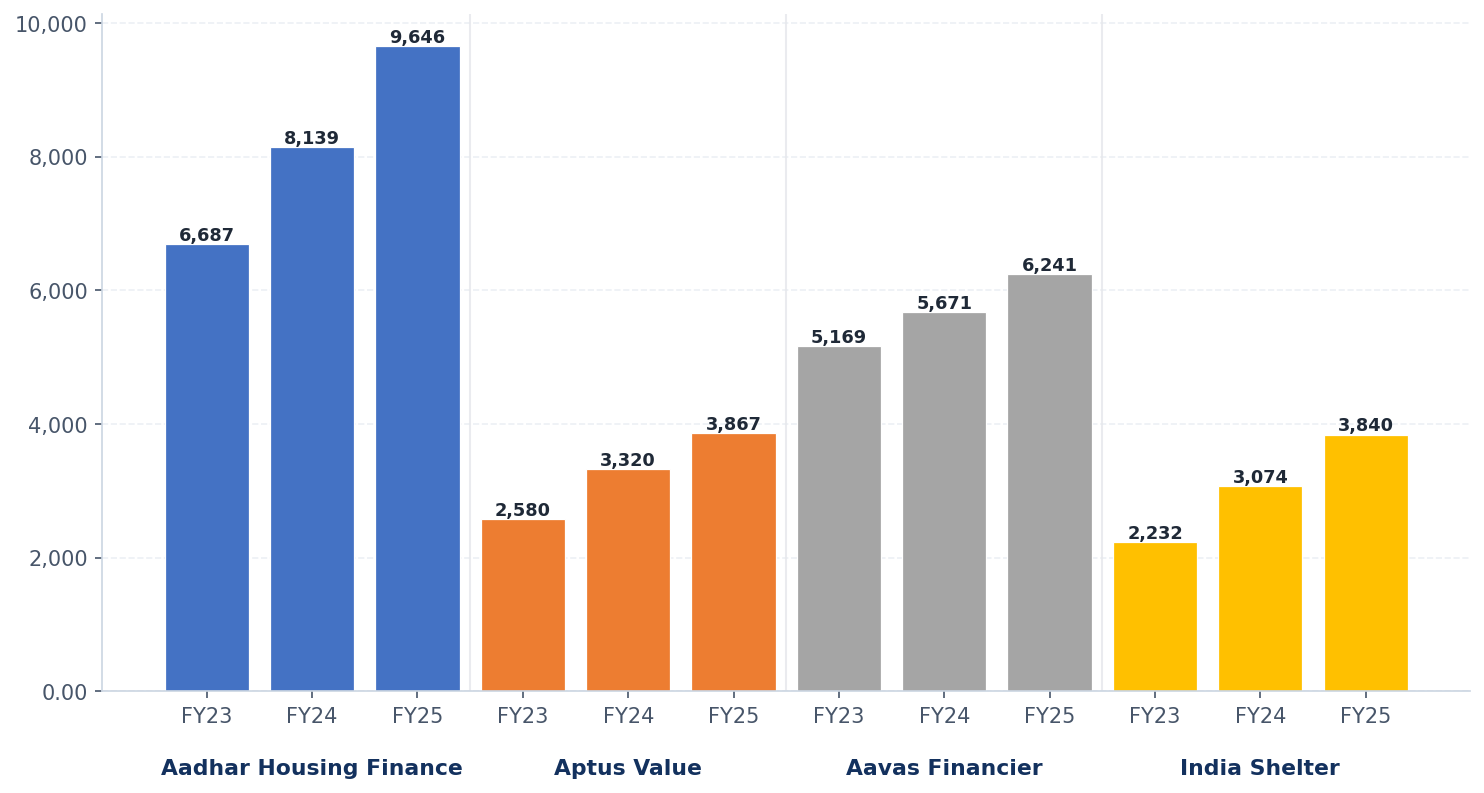

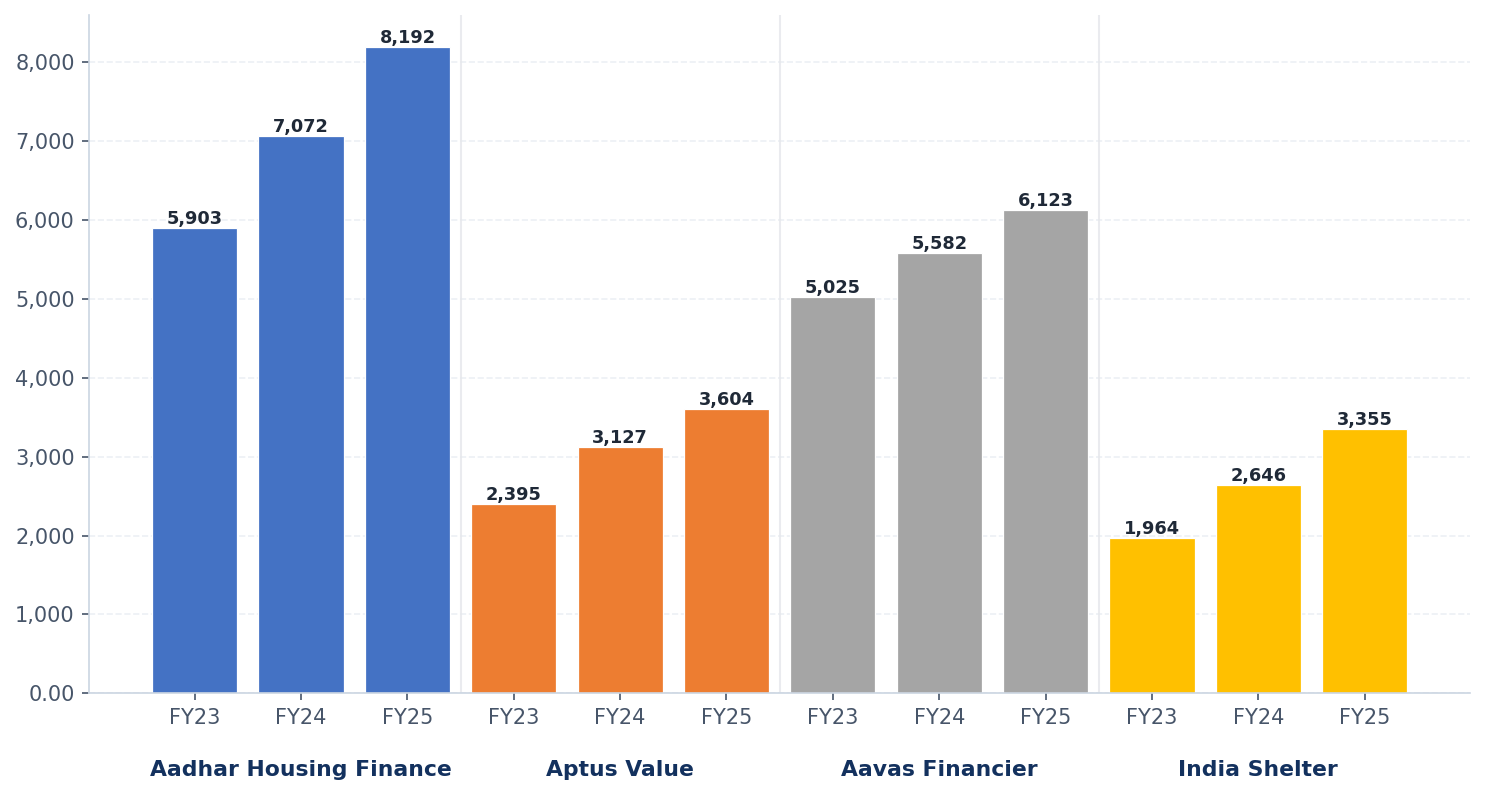

| Company Name | CMP | MCap (Rs in Cr) | AUM (Rs in Cr) (9MFY26) | P/E (TTM) | P/BV (TTM) | ROA (9MFY26) | ROE (9MFY26) | GNPA (9MFY26) | NNPA (9MFY26) |

|---|---|---|---|---|---|---|---|---|---|

| Aadhar Housing Finance | 480.60 | 20,954 | 28,790 | 20.20 | 3.02 | 4.40% | 15.60% | 1.40% | 1.00% |

| Aptus Value | 230.66 | 11,556 | 12,330 | 12.96 | 2.48 | 7.90% | 20.00% | 1.56% | 1.18% |

| Aavas Financier | 1,293.00 | 10,253 | 22,204 | 16.33 | 2.19 | 3.25% | 13.71% | 1.19% | 0.79% |

| India Shelter | 794.80 | 8,663 | 10,365 | 18.16 | 2.97 | 5.90% | 16.90% | 1.50% | 1.20% |

*CMP & MCap are as per 15th April, 2026.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

Year of incorporation of Aadhar Housing Finance Pvt. Ltd. (AHFPL) in Lucknow.

Opened the 15th Branch and crossed 1000 home loan disbursements.

AUM crossed of Rs 10 billion.

Opened 100th branch & Customer base reached 49,000.

Merger of DHFL Vysya Housing Finance Ltd with AHFPL.

AUM crossed Rs 100 billion and the company raised Rs 7 billion through maiden public offering of NCDs.

The customer base crossed 150k, while BCP Topco (Blackstone) infused Rs 14.4 billion in the company and acquired the company in Jun'19.

Branches reached 580 and the AUM crossed Rs 255 billion.

The customer base stood at 324,000, while the branches count stood at 621 and the AUM crossed Rs 287 billion.

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026

SCORE: 7

SCORE: 6

SCORE: 8

SCORE: 5

Sources: CSEC Research, Company Filings, NSE, BSE • Date: 16th April, 2026